BLOG

In make-to-stock production manufacturing orders collect costs. Materials are produced based on a production plan by material requirements planning (MRP), not based on customer demand.

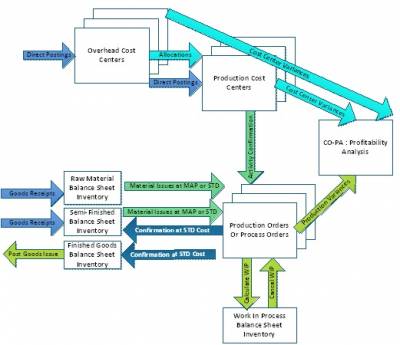

Accounting documents are posted throughout the month to both overhead and production cost centers in a plant. These are known as direct postings.

Costs are planned by cost center to determine plan vs. actuals, variances, under/over absorption, and activity rates used in production. You can see the cost center variances in Figure 1 that are determined when direct postings are accumulated and these variances can be posted to CO-PA. Cost center variances result from under or over absorption of overhead costs and production cost center’s resources.

Assessments and distributions are where you send overhead costs to production cost centers to be included in the plan vs. actual comparison and activity rate calculation.

A green arrow in Figure 1 from Production Cost Centers to Production Orders shows Activity Confirmations, where the activity rates set up in production cost centers are used when activities are confirmed on orders. The work center’s production cost center is credited and the order is debited for activity usage.

As materials are received, a goods receipt posting is made to raw material or semi-finished goods inventory on the balance sheet. Any purchase price variance for a standard cost item is posted to a P&L purchase price variance (PPV) account. PPV’s can be analyzed and capitalized to the balance sheet if desired. When materials are backflushed or issued to production, they are issued at their MAP or standard cost depending on price control. The order is debited for the material expense and the inventory account is credited.

Figure 1: Make-To-Stock Cost Flow

As materials are produced on an order, they are confirmed and posted to semi-finished good or finished good inventory on the balance sheet. When materials are sold to a customer, a post goods issue posting is made to credit inventory.

If an order is not status TECO or DLV at month end, meaning the order is not yet complete, it goes through WIP calculation. When an order is TECO or DLV in a subsequent month, the WIP balance is canceled and production variances are settled to COPA.

For the latest updates

Tanya Duncan is Senior Manager at Deloitte Consulting, the world's largest private professional services firm. She previously worked for Owens Corning, a Fortune 500 global building materials company in Toledo, OH. She is experienced in global SAP deployments and has authored SAP books:

Tanya Duncan is Senior Manager at Deloitte Consulting, the world's largest private professional services firm. She previously worked for Owens Corning, a Fortune 500 global building materials company in Toledo, OH. She is experienced in global SAP deployments and has authored SAP books:

Comments 1

I found a little mistake: "When materials are sold to a customer, a post goods issue posting is made to debit inventory."

I believe to credit inventory