By John Jordan

What's the difference between process and production orders in SAP S/4HANA?

SAP process orders provide more functionality than production orders, including phases and process instructions for process industries.

When you create production orders, a routing and a bill of material (BOM) are transferred to the master data of the order header. When you manufacture with process orders, the master recipe and associated materials list are transferred. The difference occurs because process industries manufacture in phases, converting initial liquid batches into consumable batches, bottled and packaged.

There are no costing differences between process and production orders; however, there are differences in terminology and production functionality. Let's explore these.

You maintain a process order with the Manage Process Orders app (SAP Fiori ID F4587)

You can also maintain process orders with SAP GUI Transaction COR2 or via menu path:

Logistics - Production - Process - Process Order - Display

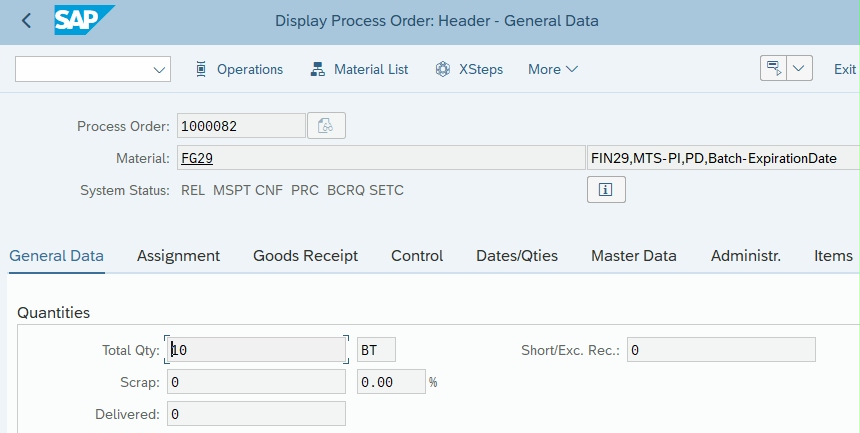

A process order is displayed, as shown in Figure 1.

Figure 1 Display Process Order

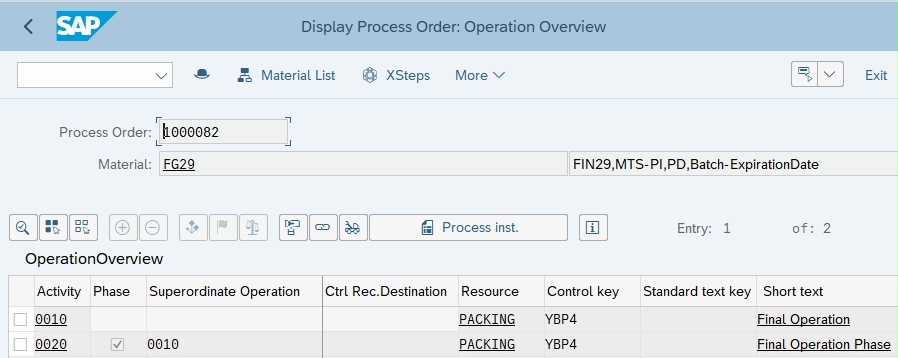

Click the Operations button at the top to display the Operation Overview, as shown in Figure 2.

Figure 2 Process Order Operation Overview

A process order contains operations divided into phases. A phase is a self-contained work step that defines the detail of one part of the production process using the primary resource of the operation. A resource is similar in concept to a work center and is assigned to a cost center. The cost center assigns activity types to the resource.

In process manufacturing, only phases are costed, not operations. A phase is assigned to a superordinate operation and contains standard activity values to determine dates, capacity requirements, and costs. The Relevancy to Costing Indicator in the phase must be selected as shown in Figure 3.

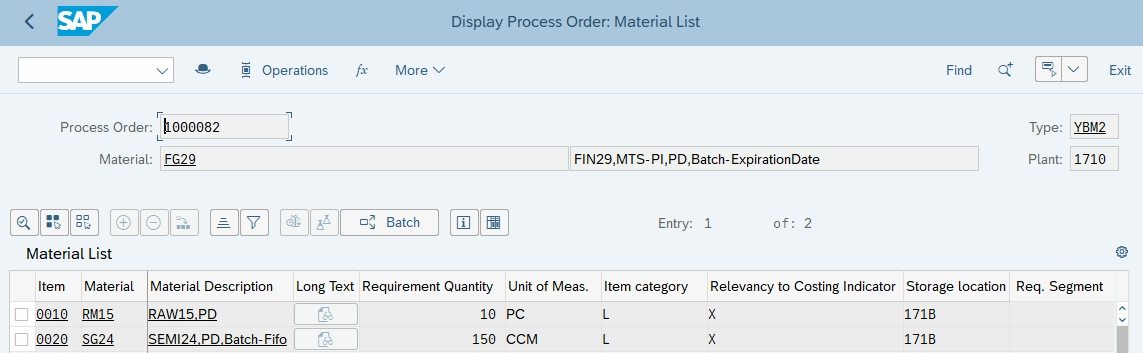

Materials are required for the execution of each step in each operation or phase you plan. Raw materials and semi-finished products that enter the production process debit the manufacturing order as they are withdrawn from inventory. Click the Materials List button in Figure 2 to display the materials, as shown in Figure 3.

Figure 3 Process Order Material List

Intra Materials

Intra materials, including INTRA, are temporary and only exist between production phases. Intra materials appear in the material lists as items of category M and are not costed. If the process is interrupted because of a malfunction, however, an intra material may have to be put into inventory. In this case, it's valuated with a price in the material master.-

Remaining Materials

The remaining materials are represented as by-products. A by-product is an incidental output of a joint process. You enter a by-product with a negative quantity in the primary product's or process material's materials list. You don't select the Co-Product indicator for by-products in the material master or the BOM.

Circulating Materials

Circulating materials, such as catalysts, can be both a process input and a process output. You can specify in the material list whether the costs for a circulating material should be considered. The system selects a price for the circulating material from the material master. If the circulating material is flagged as relevant to costing, the material costs appear in the itemization twice: once with a plus sign and once with a minus sign. The balance is the material input cost.

Co-Products

If the materials list contains co-products, you can add additional co-products. You cannot, however, delete co-products from the materials list. To see if a material component is relevant to costing, go from the materials list to the detail screen for the material. All co-products (leading and non-leading) are items with a negative quantity. Leading co-products are called primary products.

You maintain process instructions (PI) for phases by clicking the Operations button in the header screen of a process order, selecting a phase, and choosing Operation—Process Instruction Overview from the menu bar.

You've been reading Tip #50

Keep reading 110 SAP S/4HANA tips click here: 110 Things You Should Know About Controlling with SAP

Save 15% with your personal coupon code JORDAN15

Many companies buy multiple copies for project teams

What readers are saying about this book:

- Best SAP shortcuts save me a lot of time, and it's fun to read!

- John's book has paid for itself many times over

- My colleagues appreciate me for sharing these valuable ideas

- I like the SAP Material Ledger conversion and go-live ideas that saved three months of preparation time before a very smooth go-live

Glossary

Accrual Order

An accrual order enables you to monitor period-related accrual calculations between expenses posted in financial accounting and controlling.

Active Pharmaceutical Ingredient API

An active pharmaceutical ingredient (API) is the substance in a drug that is pharmaceutically active and is by far the highest-cost ingredient. One way to identify these costs is with a separate cost component by creating an API origin group and assigning it to API material masters with Transaction MM02 and an API cost component in the cost component structure with Transaction OKTZ.

Activity-Based Costing

While you typically allocate overhead costs during activity-type confirmations or with costing sheets, templates offer a more flexible alternative. Although setting up templates is more complex, they are set out logically and are worth considering as a flexible alternative for overhead costs.

Activity Input Planning

Cost centers provide planned output services based on activity quantities with Transaction KP26. You can plan cost center activity input quantities from other cost centers with activity input planning using Transaction KP06.

Activity Type

An activity type identifies activities provided by a cost center to manufacturing orders. The secondary cost element associated with an activity type identifies the activity costs on cost center and detailed reports.

Actual Costing

Actual costing determines what portion of the variance is debited to the next-highest level using material consumption. All purchasing and manufacturing difference postings are allocated.

Backflushing

Backflushing is the automatic posting of a goods issue for components after their actual physical issue for use in an order. The goods issue posting of backflushed components is carried out automatically during confirmation.

Backflushing reduces the amount of work in warehouse management, especially for low-value parts. The material components from the BOM required in the operation should be assigned to the operations in the routing.

Bill of Material

A bill of material (BOM) is a structured hierarchy of components necessary to build an assembly. BOMs and purchasing info records provide cost estimates with the information necessary to calculate the material costs of assemblies.

By-Product

A by-product is a product that is produced in conjunction with other products. The system does not create a separate order item for each by-product. The material valuation of a by-product is always based on the price specified by price control in the material master. If a by-product is indicated as being relevant to costing in BOM, the total cost of the process is reduced by the costs of the by-products

Co-Product

You select the co-product indicator in the MRP 2 and Costing 1 views if a material is a valuated product produced simultaneously with one or more other products. Setting this indicator allows you to assign the proportion of costs this material will receive about other co-products within an apportionment structure.

Backflush

Backflushing is automatically posting a goods issue for components in an order during confirmation. It reduces the amount of work in warehouse management, especially for low-value parts. The material components from the BOM are assigned to operations in the routing.

Base Quantity

All component quantities in a BOM relate to the base quantity. Increasing the base quantity increases the accuracy of component quantities, similar to the price unit.

Base Unit of Measure

Material stocks are managed in the base unit of measure. The system converts all quantities you enter in other units of measure (alternative units) to the base unit of measure.

Bill of Material

A bill of material (BOM) is a structured hierarchy of components necessary to build an assembly. BOMs and purchasing info records allow cost estimates to calculate assembly material costs.

BOM Application

A BOM application is a costing variant component for automatically determining alternative BOMs.

BOM Group

A BOM group is a collection of BOMs for a product or number of similar products.

BOM Item Component Quantity

The quantity of a BOM item that is entered in relation to the base quantity of the product.

BOM Item Status

Six indicators, such as costing relevancy, are contained in the Status/Long Text tab of a BOM item.

BOM Status

This controls the current processing status of the BOM. For example, a BOM may have a default status of not active when initially created, which then may be changed to active when the BOM is available for use in material requirements planning (MRP) and released for planned orders.

BOM Usage

This determines a section of your company, such as production, engineering, or costing. You define which item statuses can be used in each BOM usage; for example, all items in BOMs with a certain usage may be relevant to production.

Bulk Material

Bulk materials are not relevant for costing in a cost estimate and are expensed directly to a cost center. The Bulk Material checkbox is maintained in the MRP 2 view and the BOM item. If a material is always used as a bulk material, set the indicator in the material master. If a material is only used as a bulk material in individual cases, the indicator set in the BOM item has a higher priority.

Calculation Base

A calculation base is a group of cost elements to which overhead is applied. It is a component of a costing sheet that summarizes the rules for allocating overhead.

Chart of Accounts

A chart of accounts is a group of general ledger accounts assigned to each company code. It is the operative chart of accounts used in financial and cost accounting. All companies within the one controlling area must have the same operative chart of accounts. Other charts of accounts include the country-specific chart of accounts required by individual country legal requirements and the group chart of accounts required by consolidation reporting.

Company Code

A company code is the smallest organizational unit of financial accounting for

which a complete self-contained chart of accounts can be drawn up for external reporting.

Component Scrap

Component scrap is the percentage of component quantity that does not meet required quality standards before being inserted in the production process. The plan quantity of components is increased. Component scrap is an input scrap because it is detected before use in the production process. You can plan component scrap in the MRP 4 view and the Basic Data tab of the BOM item. An entry in the BOM item field takes priority over an entry in the material master MRP 4 view.

Condition

Conditions are stipulations agreed upon with vendors, such as prices, discounts, surcharges, freight, duty, and insurance. You maintain purchasing conditions in quotations, purchasing info records, outline agreements, and orders.

Condition Technique

The condition technique is used to determine the purchase price by consideration of all the relevant pricing elements. A feature of the technique is the formulation of rules and requirements.

Condition Type

A condition type is a key that identifies a condition. The condition type indicates, for example, whether the system applies a price, a discount, a surcharge, or other pricing, such as freight costs and sales taxes.

Confirmation

A confirmation documents the processing status of orders, operations, and individual capacities. You specify the operation yield, scrap and rework quantity, the activity quantity, work center, and who performed the operation.

Consignment Material

Consignment occurs when a vendor maintains a stock of materials at a customer site. The vendor retains ownership of the materials until they are withdrawn from the consignment stores.

Cost Center

A cost center is master data that identifies where the cost occurred. A responsible person assigned to the cost center analyzes and explains cost center variances at period end.

Cost Component

A cost component identifies costs of similar types, such as material, labor, and overhead costs by grouping together cost elements in the cost component structure.

Cost Component Group

Cost component groups allow you to display cost components in standard reports. In the simplest implementation, you create a cost component group for each cost component and assign each group to a corresponding cost component. You assign cost component groups as columns in cost estimate list reports and costed multilevel BOMs.

Cost Component Split

The cost component split is the combination of cost components that makes up the total cost of a material. For example, if you need to view three cost components (material, labor, and overhead) for your reporting requirements, the combination of these three cost components represents the cost component split.

Cost Component Structure

You define which cost components make up a cost component split by assigning them to a cost component structure. Within the cost component structure, you assign cost elements and origin groups to cost components.

Cost Component View

Each cost component is assigned to a cost component view. When you display a cost estimate, you can choose a cost component view, which filters the cost components displayed in the cost estimate.

Cost Element

Cost elements are included as part of a general ledger account. Primary cost elements identify external costs, while secondary cost elements identify costs allocated within controlling, such as activity allocations from cost centers to manufacturing orders.

Cost Estimate

A cost estimate calculates the plan cost to manufacture a product or purchase a component. It determines material costs by multiplying BOM quantities by the standard price, labor costs by multiplying operation standard quantities by plan activity price, and overhead by costing sheet configuration.

Costed Multilevel BOM

A costed multilevel BOM is a hierarchical overview of the values of all items of a costed material according to the material?s costed quantity structure (BOM and routing). You display a costed multilevel BOM on the left side of a cost estimate screen. You can also view a costed multilevel BOM separately with Transaction CK86_99.

Event-Based Processing

As of SAP S/4HANA release 2022, event-based processing is available, where goods movements and confirmations represent events that trigger the calculation of overhead according to the costing sheet. Then, depending on the status of the order, this triggers either the posting of a journal entry for the work in process (WIP) or the cancellation of any existing WIP and the calculation of production variances.

Goods Issue

A goods issue is the movement (removal) of goods or materials from inventory to manufacturing or to a customer. When goods are issued, it reduces the number of stock in the warehouse.

GR/IR

GR/IR is the SAP process to execute the three-way match- purchase order, Material Receipt, as well as vendor invoice. You use a clearing account to record the offset of the Goods Receipt (GR) and Invoice Receipt (IR) postings. As soon as completely processed, the postings in the cleaning account balance.

Internal Order

An internal order monitors costs and revenue of an organization for short- to-medium-term jobs. You can carry out planning at a cost element and detailed level, and budgeting at an overall level with availability control.

Long-Term Planning

Long-term planning allows you to enter medium- to longer-term production plans, and simulate future production requirements with long-term MRP. You can determine future purchasing requirements for vendor RFQs, update purchasing info records, and transfer planned activity requirements to cost center accounting.

Margin Analysis

Margin Analysis is the refined version of Account-based COPA. The Universal Journal combines financial and managerial accounting and directly records all dimensions, including custom fields. Margin Analysis provides consistent financial information without any reconciliation needs along with a financial audit trail. All innovations developed for the Universal Journal are immediately available within Margin Analysis. A consistent approach ensures common usage of ledgers, currencies, valuations, predictions, and simulations, as well as their availability in planning and reporting.

Master Data

Master data is information that stays relatively constant over long periods of time. For example, purchasing info records contain vendor information such as a business name, which usually doesn't change.

Material Master

A material master contains all the information required to manage a material. Information is stored in views, and each view corresponds to a department or area of business responsibility. Views conveniently group information together for users in different departments, for example, sales and purchasing.

Process Order

A process order is a manufacturing order that is used in process industries. A master recipe and materials list are copied from master data to the order. A process order contains operations that are divided into phases. A phase is a self-contained work-step that defines the detail of one part of the production process using a primary resource.

In process manufacturing, only phases are costed not operations. A phase is assigned to a subordinate operation and contains standard values for activities, which are used to determine dates, capacity requirements, and costs.

Procurement Alternative

A procurement alternative represents one of a number of different ways of procuring a material. You can control the level of detail in which the procurement alternatives are represented through the controlling level. Depending on the processing category, there are single-level and multilevel procurement alternatives. For example, a purchase order is single-level procurement, while production is multilevel procurement.

Production Order

A production order is used for discrete manufacturing. A BOM and routing are copied from master data to the order. A sequence of operations is supplied by the routing, which describes how to carry out work-steps.

An operation can refer to a work center at which it is to be performed. An operation contains planned activities required to carry out the operation. Costs are based on the material components and activity price multiplied by a standard value.

Product Drilldown Reports

Product drilldown reports allow you to slice and dice data based on characteristics such as product group, material, plant, cost component, and period. Product drilldown reports are based on predefined summarization levels and are relatively simple to setup and run.

Production Variance

Production variance is a type of variance calculation based on the difference between net actual costs debited to the order and target costs based on the preliminary cost estimate and quantity delivered to inventory. You calculate production variance with target cost version 1. Production variances are for information only and are not relevant for settlement.

Production Version

A production version determines which alternative BOM is used together with which task list/master recipe to produce a material or create a master production schedule. For one material, you can have several production versions for various validity periods and lot-size ranges.

Purchase Price Variance

When raw materials are valued at the standard price, a purchase price variance will post during goods receipt if the goods receipt or invoice price is different from the material standard price.

Profitability Analysis

Costing-based profitability analysis enables you to evaluate market segments, which can be classified according to products, customers, orders (or any combination of these), or strategic business units, such as sales organizations or business areas concerning your company's profit or contribution margin.

Profit Center

SAP Profit Center is a management-oriented organizational unit used for internal controlling purposes. Segmenting a company into profit centers allows us to analyze and delegate responsibility to decentralized units.

Purchasing Info Record

A purchasing info record stores all the information relevant to the procurement of a material from a vendor. It contains the Purchase Price field, which the standard cost estimate searches for when determining the purchase price.

Raw Materials

Raw materials are always procured externally and then processed. A material master record of this type contains purchasing data but not sales.

Routing

A routing is a list of tasks containing standard activity times required to perform operations to build an assembly. Routings, together with planned activity prices, provide cost estimates with the information necessary to calculate labor and activity costs of products.

Sales and Operations Planning

Sales and operations planning (SOP) allows you to enter a sales plan, convert it to a production plan, and transfer the plan to long-term planning.

S&OP is slowly being replaced by SAP Integrated Business Planning for Supply Chain (SAP IBP), which supports all S&OP features. S&OP is intended as a bridge or interim solution, which allows you a smooth transition from SAP ERP to on-premise SAP S/4HANA and SAP IBP. See SAP Note 2268064 for details.

SAP Fiori

SAP Fiori is a web-based interface that can be used in place of the SAP GUI. SAP Fiori apps access the Universal Journal directly, taking advantage of additional fields like the work center and operation for improved variance reporting.

Settlement

Work in process (WIP) and variances are transferred to Financial Accounting, Profit Center Accounting (PCA), and Profitability Analysis (CO-PA) during settlement. Variance categories can also be transferred to value fields in CO-PA.

Settlement Profile

A settlement profile contains the parameters necessary to create a settlement rule for manufacturing orders and product cost collectors and is contained in the order type.

Settlement Rule

A settlement rule determines which portions of a sender's costs are allocated to which receivers. A settlement rule is contained in a manufacturing order or product cost collector header data.

Setup Time

You need setup time to prepare equipment and machinery for the production of assemblies, and that preparation is generally the same regardless of the quantity produced. Setup time spread over a smaller production quantity increases the unit cost.

Simultaneous Costing

The process of recording actual costs for cost objects, such as manufacturing orders and product cost collectors in cost object controlling, is called simultaneous costing. Costs typically include goods issues, receipts to and from an order, activity confirmations, and external service costs.

Source Cost Element

Source cost elements identify costs that debit objects, such as manufacturing orders and product cost collectors.

Source List

A source list is a list of available sources of supply for a material, which indicates the periods during which procurement is possible. Usually, a source list is a list of quotations for a material from different vendors.

You can specify a preferred vendor by selecting a fixed source of supply indicator. If you do not select this indicator for any source, a cost estimate will choose the lowest cost source as the cost of the component. You can also indicate which sources are relevant to MRP.

Standard Price

The standard price in the Costing 2 view determines the inventory valuation price when price control is set at standard (S). The standard price is updated when a standard cost estimate is released. You normally value manufactured goods at the standard price.

Subcontracting

You supply component parts to an external vendor who manufactures the complete assembly. The vendor has previously supplied a quotation, which is entered in a purchasing info record with a category of subcontracting.

Tracing Factor

Tracing factors determine the cost portions received by each receiver from senders during periodic allocations, such as assessments and distributions.

Universal Journal

The efficiency and speed of the SAP HANA in-memory database allowed the introduction of the Universal Journal single line-item tables ACDOCA (actual) and ACDOCP (plan). The Universal Journal allows all postings from the previous financial and controlling components to be combined in single items. The many benefits include the development of real-time accounting. In this book, we discuss both period-end and event-based processing.

Valuation Class

The valuation class in the Costing 2 view determines which general ledger accounts are updated as a result of inventory movement or settlement.

Valuation Date

The valuation date determines which material and activity prices are selected when you create a cost estimate. Purchasing info records can contain different vendor-quoted prices for different dates. Different plan activity rates can be entered per fiscal period.

Valuation Grouping Code

The valuation grouping code allows you to assign the same general ledger account assignments across several plants with Transaction OMWD to minimize your work.

The grouping code can represent one or a group of plants.

Valuation Type

You use valuation types in the split valuation process, which enables the same material in a plant to have different valuations based on criteria such as batch. You assign valuation types to each valuation category, which specify the individual characteristics that exist for that valuation category. For example, you can valuate stocks of a material produced in-house separately from stocks of the same material purchased externally from vendors. You then select procurement type as the valuation category and internal and external as the valuation types.

Valuation Variant

The valuation variant is a costing variant component that allows different search strategies for materials, activity types, subcontracting, and external processing. For example, the search strategy for purchased and raw materials typically searches first for a price from the purchasing info record.

Valuation Variant for Scrap and WIP

This valuation variant allows a choice of cost estimates to valuate scrap and WIP in a WIP at target scenario. If the structure of a routing is changed after a costing run, WIP can still be valued with the valuation variant for scrap and WIP resulting in a more accurate WIP valuation.

Valuation View

In the context of multiple valuation and transfer prices, you can define the following views:

- Legal valuation view

- Group valuation view

- Profit center valuation view

Work Center

Operations are carried out at work centers representing; for example, machines, production lines, or employees. Work center master data contains a mandatory cost center field. A work center can only be linked to one cost center, while a cost center can be linked to many work centers.

Work in Process

Work in process (WIP) represents production costs of incomplete assemblies. For balance sheet accounts to accurately reflect company assets at period end, WIP costs are moved temporarily