BLOG

Objects that no longer exist have no value. Therefore, you must check the existence of fixed assets by means of a physical inventory. The individual objects in fixed assets must be recorded so they are identifiable.

The inventory is the record (directory) of individual asset objects. This directory must report the asset objects present on a specified date. These objects must be determined by a physical check, also known as a physical inventory. The word inventory is derived from the Latin invenire, meaning to find something. In this blog I explain what you have to list in the fixed assets inventory and how to perform the physical check.

National tax and accounting laws regulate the information the inventory directory must contain. These laws also regulate how and at what time intervals a physical inventory must take place.

You verify that the individual assets listed in the inventory directory are present by a physical inventory, meaning the assets should be viewed and counted individually—which can be a very time-consuming measure.

Accountants are often accused of being bean counters. Apart from the fact that this statement is not a compliment, it is also incorrect. The effort involved in checking and reporting the value of fixed assets can, and must be kept within reasonable limits. The principle of proportionality is also applicable.

You can manage identical capital goods in the inventory as one single item, and specifying the quantity. In the sense of valuation, identical means the following:

For example, 50 personal computers could be managed under one asset number. This variant for the master asset (unfortunately frequently used) will lead to more effort later in the maintenance of asset balances. For example, these 50 personal computers will not leave the company all at the same time. Time-consuming partial retirements are necessary, and they will also not be used permanently in one cost center, thus requiring extensive partial repostings instead of simple cost center changes.

This type of inventory management causes the greatest problems for a physical asset inventory. How can you determine whether all 50 computers of this asset are still present? The individual PCs cannot be identified via asset accounting. However, annual evidence by means of a physical inventory is still required. This evidence would require additional individual inventory management outside or in addition to asset accounting. Thus the company still has the administrative effort and there is therefore no benefit.

We advise against this type of inventory management. SAP Asset Accounting offers convenient functions for creating and posting this type of mass acquisition with the initial purchase. You can address these with the Hierarchy of Asset Master Records.

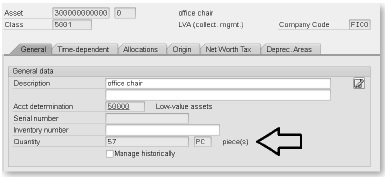

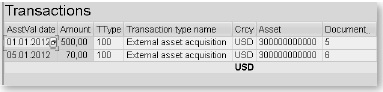

Quantity details are however still useful for certain capital goods, for example, for low-value assets that are presented as flat-rate assets. Figure 1 shows an asset with a quantity of 57 items, and Figure 2 shows the movements for this asset.

Figure 1: Asset with quantity

Figure 2: Movements for this asset

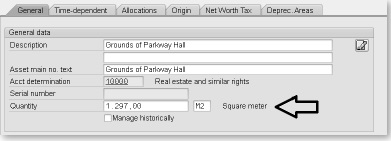

For real estate, we recommend specifying the number of square meters, as shown in Figure 3.

Figure 3: Asset with square meters

The evidence of ownership for real estate is not provided by means of a physical inventory but by the entry in the register of deeds of the corresponding plot of land number.

Jörg Siebert has 20 years of experience working with SAP Financials and is an internationally recognized author, speaker, trainer, and veteran SAP consultant. He has worked throughout Europe in the automotive, healthcare, and service industries and regularly delivers sessions at international SAP conferences. Previously, Jörg was a product manager for SAP ERP Financials at SAP German headquarters.

He is the Co-founder and Managing Director of Espresso Tutorials, a publishing company focused on short and concise SAP textbooks.

Contact Joerg at This email address is being protected from spambots. You need JavaScript enabled to view it. or on LinkedIn.

Jörg Siebert has worked as consultant, trainer and product manager  and has more than 16 years of experience with accounting software. For the last 10 years he worked at SAP Germany in Walldorf with a focus on SAP ERP Financials. He has written several books including The SAP General Ledger and SAP ERP Financials User's Guide. In 2011 he started his own publishing company www.espresso-tutorials.com - E-Books for SAP Software.

and has more than 16 years of experience with accounting software. For the last 10 years he worked at SAP Germany in Walldorf with a focus on SAP ERP Financials. He has written several books including The SAP General Ledger and SAP ERP Financials User's Guide. In 2011 he started his own publishing company www.espresso-tutorials.com - E-Books for SAP Software.

Comments