BLOG

My company is in the early stages of moving from SAP ECC 6.0 to SAP S/4HANA.

I thought it would be interesting to give you my initial impressions of what I found out about Controlling in SAP S/4HANA. Since we started out with ECC 6.0, we didn't have to worry about things like classic G/L versus new G/L.

When we first got access to an S/4HANA sandbox for a test drive, this helped me get a much better understanding of how the new system works rather than reading documentation and watching training videos. Here are my initial impressions, which may be useful if you are making the move, or considering it.

When you think about user interfaces with SAP S/4HANA, you think SAP Fiori because it is one of the main advantages. I first logged on to the S/4HANA test client with the SAPGUI interface. Whether using the SAPGUI or SAP Business Client interfaces, logging into S/4HANA looks exactly like logging into ECC 6.0. You can use existing transactions and processes.

You do not need to work through new business processes when making the transition. This makes the move more like an enhancement pack upgrade rather than a new implementation. This is not an enhancement pack upgrade and should not be treated as such. However, it's comforting to know that you can make the transition with minimal impact to end users.

S/4HANA works well with the traditional look, but the extensive use of Fiori tiles give a modern interface and provide a way of displaying real-time and predictive analytic information. I looked for tiles for production orders to show some problem orders for review. I wanted to click on a tile to display a list of orders. Unfortunately, I could not find a tile specifically for that. I found tiles that executed standard transactions (a must if you are using Fiori as your only interface) and enhanced reports. Little was available for the dashboard view I was looking for. This is not a major issue, as existing functionality remains, but I was a little disappointed in the lack of predictive analytic tools provided for the Controlling community.

The list itself is not simple – the 1709 simplification list is 906 pages long. It also appears that not everything that is listed as replaced is gone.

When I initially logged on to the S/4HANA client, I wanted to see how obsolete transactions were treated. Knowing that base planning objects were on the simplification list, I ran transaction KKE1 expecting to see either that there was no such transaction or a message indicating that KKE1 was obsolete. Instead, I found that KKE1 still worked. This was one of the transactions S/4HANA 1709 simplification lists as obsolete. However, in SAP Note 2133644 (Error message SFIN_FI 004: Transactions KKE1, KKE2, KKE3 cannot be called), it appears that even back in the days of Simple Finance (Feb 2015), this functionality was brought back into use. A few other base planning object transactions were included with these three, but several of the reports continue to be obsolete. This is despite the fact that the 1709 simplification list chapter 8.2 referring to SAP Note 2270335 (S4TWL - Replaced Transaction Codes and Programs in FIN) and again in chapter 12.1 referring to SAP Note 2349294 (S4TWL - Reference and Simulation Costing) both indicate that these transactions are replaced in S/4HANA.

Base planning objects continue to live, with the caveat that you should convert to unit costing (CKUC) or Easy Cost Planning to create ad hoc costs (SAP Note 2270335). The implication is that at some point these transactions will go away. I think that the return of base planning objects to S/4HANA is good since costs can be created without reference to a material (unit costing) or a costing model (Easy Cost Planning). Base planning objects can be used in conjunction with Easy Cost Planning to enhance the power of the tool in creating ad hoc cost estimates. I hope that SAP reconsiders whether base planning objects should be kept in future releases.

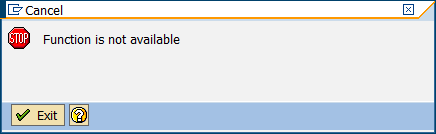

If the transaction has been removed, the transaction window is displayed with the dialog box as shown in Figure 1 with message SFIN_FI004, or the message will be displayed at the bottom of an empty window.

Figure 1 Message SFIN_FI004

Review the simplification list, and verify with testing. Some transactions on the list are gone, but others may still be available. I expect that at some point those on the list that are currently available may desappear, so plan accordingly.

The Universal Journal is the single source of truth, combining Controlling and General Ledger postings in table ACDOCA. Because of the speed of the HANA database there is no need for separate aggregate tables for period-based information. Not only is duplication of data no longer required to get reports in a timely manner, there is also no longer any problem reconciling FI and CO because all the data is kept together. You might expect that tables such as COEP for CO line items and the COSP and COSS aggregate tables for primary and secondary postings would no longer be required. In fact, all of these table names have been converted into database views so that existing reports still work without making extensive programming changes.

It is logical to conclude is that these tables are no longer required in S/4HANA. However, not only are these tables not dead, they are not even mostly dead (for Princess Bride fans), and are an integral part of the Controlling database landscape in S/4HANA. The relevant SAP Note is 2270404 (S4TWL – Technical Changes in Controlling), which is also section 12.4 of the 1709 simplification list. For any actual CO postings (value type 4), everything is stored in ACDOCA.

There are no updates to the aggregate tables for these postings. Statistical postings (value type 11) are treated the same way, but these are also updated in the old table COEP. All other value types, including plan costs (value type 1), and target costs (value type 5) are posted the same as before, using the old tables. I did test some manual activity type postings which updated the old COEP table with a new value type (U4). Although the original COEP, COSP, and COSS tables still exist in S/4HANA, because these names are used as compatibility views, the table names have changed. COSP and COSS are COSP_BAK and COSS_BAK, respectively. COEP may have an alternate table ID, but the only way to get to just the data stored in it, you need to use the view name V_COEP_ORI.

SAP Material Ledger is mandatory in S/4HANA. This does not mean that you will be forced into actual costing, but instead the underlying data structures become a necessary part of the S/4HANA landscape. The Material Ledger table structures in ECC 6.0 are complex. Moving to S/4HANA this data structure has been simplified. Of course, with simplification comes a change in functionality. According to Rogerio Faleiros, who had an excellent presentation on SAP Material Ledger in S/4HANA in the 2017 Controlling Conference (Myths vs. Fact: SAP Material Ledger in SAP S/4HANA), SAP has taken at least a small step backwards in functionality in his opinion. Some of the issues he lists may or may not apply to your situation. For example, my company does actual costing, but does not use the full set of features available with Material Ledger. I tested the actual cost run in a test S/4HANA client after posting purchase price and usage variances. The costing run transaction CKMLCP is streamlined and many defects from the earlier version, including handling locked records and materials that hadn’t closed properly in the previous costing run are resolved. In addition, several of the steps have been combined into one Settlement step, which makes it more convenient to set up and use. Of course, this streamlining comes with a price. You can no longer distinguish between single-level and multi-level differences. For details, see SAP Note 2354768: S4TWL – Technical Changes in Material Ledger with Actual Costing (section 12.3 in the 1709 simplification list). This highlights many of the changes in database structure and functionality.

What concerned me was the elimination of the distinction between single-level and multi-level differences in actual costing. This was on Rogerio Faleiros’ list of Material Ledger disappointments. I created purchase price and usage variances in the S/4HANA sandbox so that I could post differences when performing the actual costing run. The new actual costing run is easier to use and corrects some problems that CKMLCP currently has. For example, locking in the material master causes certain items to not close correctly. If these are not rerun or manually corrected with the Material Ledger helpdesk, you will not see the correct cost. This is corrected with the new Material Ledger and I'm looking forward to seeing how it performs in production. The resulting financial documents look different in S/4HANA to ECC 6.0. There are no single-level or multi-level difference postings. There is only a difference posting using accounts defined for transaction event PRV. This looks strange when reviewing accounting documents, but since we do not distinguish single-level from multi-level differences with separate G/L accounts in our implementation, this does not have a major impact. We have less information in variance analysis, but we don’t do that analysis often.

The point I wish to make is that there have been major changes in how Material Ledger works in S/4HANA, and that you should review them to see if these changes will cause you any pain when upgrading. There are some additional notes to review that are included in the 1709 simplification list. These are 2332591 or section 16.2: S4TWL – Technical Changes in Material Ledger, 2352383 or section 16.6: S4TWL – Conversion to S/4HANA Material Ledger and Actual Costing, and 2267834 or section 25.5: S4TWL – Material Ledger Obligatory for Material Valuation.

The look and feel can be the same in S/4HANA making it easier for you to make the transition. Some older transactions have disappeared, but others have been resurrected. Certain transactions are permanently gone and the lifetime of resurrected transactions may be brief.

The Universal Journal has only taken over CO actual and statistical postings, so the existing CO table structure will remain intact when moving to S/4HANA. I have not concluded whether this is a good thing or a bad thing, but it will impact what you need to migrate when converting.

The Material Ledger has been simplified, but it depends on your previous implementation to determine if you have lost or gained functionality. Plan your conversion carefully and make sure you have sufficient time for testing. In the end, you will have a very familiar, but much improved ERP experience.

Just as cost centers can provide planned output services based on activity quantities with Transaction KP26, you can plan cost center activity input quantities from other cost centers with activity input planning using Transaction KP06.

An activity type identifies activities provided by a cost center to manufacturing

orders. The secondary type general ledger account associated with an activity type identifies the activity costs on cost center and detailed reports.

Actual costing determines what portion of the variance is debited to the next-highest level using material consumption. All purchasing and manufacturing difference postings are allocated upward through the BOM to assemblies and finished goods. Variances can be rolled up over multiple production levels and company codes to the finished product.

Actual costs debit a product cost collector or manufacturing order during business transactions, for example, general ledger account postings, inventory goods movements, internal activity allocations, and overhead calculation.

An allocation structure allocates the costs incurred for a sender by cost element or cost element group, and it is used for settlement and assessment. An assignment maps a source cost element group to a settlement general ledger account.

There can be multiple methods of manufacturing an assembly, and many possible bills of materials (BOMs). The alternative BOM allows you to identify one BOM in a BOM group.

While there can only be one cost center standard hierarchy, you can create as many alternative hierarchies as you like. You create an alternative hierarchy by creating cost center groups.

This is a unit of measure defined in addition to the base unit of measure. Examples of alternative units of measure include order unit (purchasing), sales unit, and unit of issue.

An apportionment method distributes the total costs of a joint production process to the primary products. The costs of the individual primary products may vary. They are apportioned by means of an apportionment structure.

An apportionment structure defines how costs are distributed to co-products. The system uses the apportionment structure to create a settlement rule that distributes costs from an order header to the co-products. For each co-product, the system generates a further settlement rule that assigns the costs distributed to the order item to stock.

Assembly scrap is the percentage of assembly quantity that does not meet required quality standards. Assembly scrap is an output scrap because it increases the planned output quantity of items in the production process. You plan assembly scrap in the MRP 1 view using the Net ID checkbox in the Basic Data tab of a BOM item.

Automatic account assignment allows you to set a default cost center per general ledger account per plant.

You may use Base Planning Objects before there is no master data (material master, BOM, routing, master recipe) in the system.

Material stocks are managed in the base unit of measure. The system converts all quantities you enter in other units of measure (alternative units of measure) to the base unit of measure.

A bill of material (BOM) is a structured hierarchy of components necessary to build an assembly. BOMs, and purchasing info records allow cost estimates to calculate material costs of assemblies.

A BOM application is a costing variant component for automatic determination of alternative BOMs.

A BOM group is a collection of BOMs for a product or number of similar products.

The quantity of a BOM item that is entered in relation to the base quantity of the product.

Six indicators, such as costing relevancy, are contained in the Status/Long Text tab of a BOM item.

This controls the current processing status of the BOM. For example, a BOM may have a default status of not active when initially created, which then may be changed to active when the BOM is available for use in material requirements planning (MRP) and released for planned orders.

This determines a section of your company, such as production, engineering, or costing. You define which item statuses can be used in each BOM usage; for example, all items in BOMs with a certain usage may be relevant to production.

Bulk materials are not relevant for costing in a cost estimate and are expensed

directly to a cost center. The Bulk Material checkbox is maintained in the MRP 2 view and the BOM item. If a material is always used as a bulk material, set the indicator in the material master. If a material is only used as a bulk material in individual cases, set the indicator in the BOM item, which has a higher priority.

A calculation base is a group of cost elements to which overhead is applied. The calculation base is a component of a costing sheet, which summarizes the rules for allocating overhead.

Capacity category enables you to differentiate between machine and labor capacity. Machine capacity is the availability of a machine based on planned and unplanned outages and maintenance requirements. Labor capacity is the number of workers who can operate a machine at the same time.

A chart of accounts is a group of general ledger accounts assigned to each company code. This chart of accounts is the operative chart of accounts used in both financial and cost accounting. All companies within the one controlling area must have the same operative chart of accounts. Other charts of accounts include the country-specific chart of accounts required by individual country legal requirements and the group chart of accounts required by consolidation reporting.

A company code is the smallest organizational unit of financial accounting for

which a complete self-contained chart of accounts can be drawn up for external reporting.

Component scrap is the percentage of component quantity that does not meet required quality standards before being inserted in the production process. The plan quantity of components is increased. Component scrap is an input scrap because it is detected before use in the production process. You can plan component scrap in the MRP 4 view and the Basic Data tab of the BOM item. An entry in the BOM item field takes priority over an entry in the material master MRP 4 view.

Conditions are stipulations agreed upon with vendors, such as prices, discounts, surcharges, freight, duty, and insurance. You maintain purchasing conditions in quotations, purchasing info records, outline agreements, and orders.

The condition technique is used to determine the purchase price by consideration of all the relevant pricing elements. A feature of the technique is the formulation of rules and requirements.

A condition type is a key that identifies a condition. The condition type indicates, for example, whether the system applies a price, a discount, a surcharge, or other pricing, such as freight costs and sales taxes.

A confirmation documents the processing status of orders, operations, and individual capacities. You specify the operation yield, scrap and rework quantity, the activity quantity, work center, and who performed the operation.

Consignment occurs when a vendor maintains a stock of materials at a customer site. The vendor retains ownership of the materials until they are withdrawn from the consignment stores.

The controlling level determines the level of detail of procurement alternatives. The standard setting of controlling level is determined by the characteristics material/plant. You specify which characteristics are updated for the production process by the controlling level.

You select the co-product checkbox located in the MRP 2 and Costing 1 views if a material is a valuated product that is produced simultaneously with one or more other products. Setting this checkbox allows you to assign the proportion of costs this material will receive in relation to other co-products within an apportionment structure.

A cost center is master data that identifies where the cost occurred. A responsible person assigned to the cost center analyzes and explains cost center variances at period end.

A cost component identifies costs of similar types, such as material, labor, and overhead costs by grouping together cost elements in the cost component structure.

Cost component groups allow you to display cost components in standard reports. In the simplest implementation, you create a cost component group for each cost component and assign each group to a corresponding cost component. You assign cost component groups as columns in cost estimate list reports and costed multilevel BOMs.

The cost component split is the combination of cost components that makes up the total cost of a material. For example, if you need to view three cost components (material, labor, and overhead) for your reporting requirements, the combination of these three cost components represents the cost component split.

You define which cost components make up a cost component split by assigning them to a cost component structure. Within the cost component structure, you assign cost elements and origin groups to cost components.

Each cost component is assigned to a cost component view. When you display a cost estimate, you can choose a cost component view, which filters the cost components displayed in the cost estimate.

Cost elements are included as part of a general ledger account. Primary cost elements identify external costs, while secondary cost elements identify costs allocated within controlling, such as activity allocations from cost centers to manufacturing orders.

A cost estimate calculates the plan cost to manufacture a product or purchase a component. It determines material costs by multiplying BOM quantities by the standard price, labor costs by multiplying operation standard quantities by plan activity price, and overhead by costing sheet configuration.

A costed multilevel BOM is a hierarchical overview of the values of all items of a costed material according to the material’s costed quantity structure (BOM and routing). You display a costed multilevel BOM on the left side of a cost estimate screen. You can also view a costed multilevel BOM separately with Transaction CK86_99.

Costing BOMs are assigned a BOM usage of costing and are usually copied from BOMs with a usage of production. You can make adjustments to costing BOMs if you require them to be different from production BOMs. With system-supplied settings, standard cost estimates search for costing BOMs before production BOMs.

The costing lot size should be set as close as possible to actual purchase or production quantities to reduce lot size variance. Unfavorable variances may result if you create a production order for a quantity that is less than the costing lot size. You need setup time to prepare equipment and machinery for production of assemblies, and that preparation is generally the same regardless of the quantity produced. Setup time spread over a smaller production quantity increases the unit cost. This also applies to externally procured items because vendors typically quote higher unit prices for smaller quantities.

A costing run is a collective processing of cost estimates, which you maintain with Transaction CK40N.

A costing sheet summarizes the rules for allocating overhead from cost centers for cost estimates, product cost collectors, and manufacturing orders. The components of a costing sheet include the calculation base (group of cost elements), overhead rate (percentage rate applied to base), and credit key (cost center receiving credit).

The costing type determines if the cost estimate can update the standard price.

The costing variant contains information on how a cost estimate calculates the standard price. For example, it determines if either the purchasing info record price is used for purchased materials, or an estimated price is manually entered in the Planned price 1 field of the Costing 2 view.

The currency type identifies the role of the currency such as local or global.

Demand management involves planning requirement quantities and dates for assemblies, as well as defining the strategy for planning and producing/procuring a finished product.

Dependent requirements are caused by higher-level dependent and independent requirements when running MRP. Independent requirements, created by sales orders or manually planned independent requirement entries in demand management, determine lower-level dependent material requirements.

Detailed reports display cost element details of manufacturing orders and product cost collectors. You can drill down on cost elements to display line-item reports during variance analysis.

You maintain distribution rules in settlement rules in manufacturing orders and product cost collectors.

As of SAP S/4HANA release 2022, event-based processing is available, where goods movements and confirmations represent events that trigger the calculation of overhead according to the costing sheet. Then, depending on the status of the order, this triggers either the posting of a journal entry for the work in process (WIP) or the cancellation of any existing WIP and the calculation of production variances.

External processing of a manufacturing order operation is performed by an external vendor. This is distinct from subcontracting, which involves sending material parts to an external vendor who manufactures the complete assembly via a purchase order.

A goods issue is the movement (removal) of goods or materials from inventory to manufacturing or to a customer. When goods are issued, it reduces the number of stock in the warehouse.

GR/IR is the SAP process to execute the three-way match- purchase order, Material Receipt, as well as vendor invoice. You use a clearing account to record the offset of the Goods Receipt (GR) and Invoice Receipt (IR) postings. As soon as completely processed, the postings in the cleaning account balance.

An internal order monitors costs and revenue of an organization for short- to-medium-term jobs. You can carry out planning at a cost element and detailed level, and budgeting at an overall level with availability control.

Long-term planning allows you to enter medium- to longer-term production plans, and simulate future production requirements with long-term MRP. You can determine future purchasing requirements for vendor RFQs, update purchasing info records, and transfer planned activity requirements to cost center accounting.

Margin Analysis is the refined version of Account-based COPA. The Universal Journal combines financial and managerial accounting and directly records all dimensions, including custom fields. Margin Analysis provides consistent financial information without any reconciliation needs along with a financial audit trail. All innovations developed for the Universal Journal are immediately available within Margin Analysis. A consistent approach ensures common usage of ledgers, currencies, valuations, predictions, and simulations, as well as their availability in planning and reporting.

Master data is information that stays relatively constant over long periods of time. For example, purchasing info records contain vendor information such as a business name, which usually doesn’t change.

A material master contains all the information required to manage a material. Information is stored in views, and each view corresponds to a department or area of business responsibility. Views conveniently group information together for users in different departments, for example, sales and purchasing.

A process order is a manufacturing order that is used in process industries. A master recipe and materials list are copied from master data to the order. A process order contains operations that are divided into phases. A phase is a self-contained work-step that defines the detail of one part of the production process using a primary resource.

In process manufacturing, only phases are costed not operations. A phase is assigned to a subordinate operation and contains standard values for activities, which are used to determine dates, capacity requirements, and costs.

A procurement alternative represents one of a number of different ways of procuring a material. You can control the level of detail in which the procurement alternatives are represented through the controlling level. Depending on the processing category, there are single-level and multilevel procurement alternatives. For example, a purchase order is single-level procurement, while production is multilevel procurement.

A production order is used for discrete manufacturing. A BOM and routing are copied from master data to the order. A sequence of operations is supplied by the routing, which describes how to carry out work-steps.

An operation can refer to a work center at which it is to be performed. An operation contains planned activities required to carry out the operation. Costs are based on the material components and activity price multiplied by a standard value.

Product drilldown reports allow you to slice and dice data based on characteristics such as product group, material, plant, cost component, and period. Product drilldown reports are based on predefined summarization levels and are relatively simple to setup and run.

Production variance is a type of variance calculation based on the difference between net actual costs debited to the order and target costs based on the preliminary cost estimate and quantity delivered to inventory. You calculate production variance with target cost version 1. Production variances are for information only and are not relevant for settlement.

When raw materials are valued at the standard price, a purchase price variance will post during goods receipt if the goods receipt or invoice price is different from the material standard price.

Costing-based profitability analysis enables you to evaluate market segments, which can be classified according to products, customers, orders (or any combination of these), or strategic business units, such as sales organizations or business areas concerning your company’s profit or contribution margin.

SAP Profit Center is a management-oriented organizational unit used for internal controlling purposes. Segmenting a company into profit centers allows us to analyze and delegate responsibility to decentralized units.

A purchasing info record stores all the information relevant to the procurement of a material from a vendor. It contains the Purchase Price field, which the standard cost estimate searches for when determining the purchase price.

Raw materials are always procured externally and then processed. A material master record of this type contains purchasing data but not sales.

A routing is a list of tasks containing standard activity times required to perform operations to build an assembly. Routings, together with planned activity prices, provide cost estimates with the information necessary to calculate labor and activity costs of products.

Sales and operations planning (SOP) allows you to enter a sales plan, convert it to a production plan, and transfer the plan to long-term planning.

SAP Fiori is a web-based interface that can be used in place of the SAP GUI. SAP Fiori apps access the Universal Journal directly, taking advantage of additional fields like the work center and operation for improved variance reporting.

Work in process (WIP) and variances are transferred to Financial Accounting, Profit Center Accounting (PCA), and Profitability Analysis (CO-PA) during settlement. Variance categories can also be transferred to value fields in CO-PA.

A settlement profile contains the parameters necessary to create a settlement rule for manufacturing orders and product cost collectors and is contained in the order type.

A settlement rule determines which portions of a sender’s costs are allocated to which receivers. A settlement rule is contained in a manufacturing order or product cost collector header data.

You need setup time to prepare equipment and machinery for the production of assemblies, and that preparation is generally the same regardless of the quantity produced. Setup time spread over a smaller production quantity increases the unit cost.

The process of recording actual costs for cost objects, such as manufacturing orders and product cost collectors in cost object controlling, is called simultaneous costing. Costs typically include goods issues, receipts to and from an order, activity confirmations, and external service costs.

Source cost elements identify costs that debit objects, such as manufacturing orders and product cost collectors.

A source list is a list of available sources of supply for a material, which indicates the periods during which procurement is possible. Usually, a source list is a list of quotations for a material from different vendors.

You can specify a preferred vendor by selecting a fixed source of supply indicator. If you do not select this indicator for any source, a cost estimate will choose the lowest cost source as the cost of the component. You can also indicate which sources are relevant to MRP.

The standard price in the Costing 2 view determines the inventory valuation price when price control is set at standard (S). The standard price is updated when a standard cost estimate is released. You normally value manufactured goods at the standard price.

You supply component parts to an external vendor who manufactures the complete assembly. The vendor has previously supplied a quotation, which is entered in a purchasing info record with a category of subcontracting.

Tracing factors determine the cost portions received by each receiver from senders during periodic allocations, such as assessments and distributions.

Unit costing is a type of spreadsheet that, due to its integration, can use existing master data and prices in the system, such as activity prices from Cost Center Accounting. You can use the spreadsheet to create totals, subtotals, and formulas for mathematical operations.

The efficiency and speed of the SAP HANA in-memory database allowed the introduction of the Universal Journal single line-item tables ACDOCA (actual) and ACDOCP (plan). The Universal Journal allows all postings from the previous financial and controlling components to be combined in single items. The many benefits include the development of real-time accounting. In this book, we discuss both period-end and event-based processing.

The valuation class in the Costing 2 view determines which general ledger accounts are updated as a result of inventory movement or settlement.

The valuation date determines which material and activity prices are selected when you create a cost estimate. Purchasing info records can contain different vendor-quoted prices for different dates. Different plan activity rates can be entered per fiscal period.

The valuation grouping code allows you to assign the same general ledger account assignments across several plants with Transaction OMWD to minimize your work.

The grouping code can represent one or a group of plants.

You use valuation types in the split valuation process, which enables the same material in a plant to have different valuations based on criteria such as batch. You assign valuation types to each valuation category, which specify the individual characteristics that exist for that valuation category. For example, you can valuate stocks of a material produced in-house separately from stocks of the same material purchased externally from vendors. You then select procurement type as the valuation category and internal and external as the valuation types.

The valuation variant is a costing variant component that allows different search strategies for materials, activity types, subcontracting, and external processing. For example, the search strategy for purchased and raw materials typically searches first for a price from the purchasing info record.

This valuation variant allows a choice of cost estimates to valuate scrap and WIP in a WIP at target scenario. If the structure of a routing is changed after a costing run, WIP can still be valued with the valuation variant for scrap and WIP resulting in a more accurate WIP valuation.

In the context of multiple valuation and transfer prices, you can define the following views:

– Legal valuation view

– Group valuation view

– Profit center valuation view

Operations are carried out at work centers representing; for example, machines, production lines, or employees. Work center master data contains a mandatory cost center field. A work center can only be linked to one cost center, while a cost center can be linked to many work centers.

Work in process (WIP) represents production costs of incomplete assemblies. For balance sheet accounts to accurately reflect company assets at period end, WIP costs are moved temporarily to WIP balance sheet and profit and loss accounts. WIP is canceled during period-end processing following delivery of assemblies to inventory.

For the latest updates

![]() Tom King recently retired from Milliken, a leading global manufacturer of specialty textiles, floor covering, and chemicals based in Spartanburg, South Carolina. He was lead SAP CO analyst and has more than 30 years of experience in manufacturing and product costing. Tom has published three SAP books with Espresso Tutorials:

Tom King recently retired from Milliken, a leading global manufacturer of specialty textiles, floor covering, and chemicals based in Spartanburg, South Carolina. He was lead SAP CO analyst and has more than 30 years of experience in manufacturing and product costing. Tom has published three SAP books with Espresso Tutorials:

- Practical Guide to SAP CO Templates

- SAP S/4HANA Product Cost Planning Configuration and Master Data

- SAP S/4HANA Product Cost Planning Costing with Quantity Structure

Comments 1

Nice and well planned blog

Love reading the information.