BLOG

Category 2 activity types are for indirect determination and indirect allocation.

Figure 1 Display Activity Type Category 2 Transaction KL03

You cannot make direct postings for category 2 activity types with transaction KB21N, which is reserved for category 1 activity types. Instead, you must set up an indirect activity allocation cycle, which calculates the activity quantities and various receivers that can accept the allocations from the activity postings.

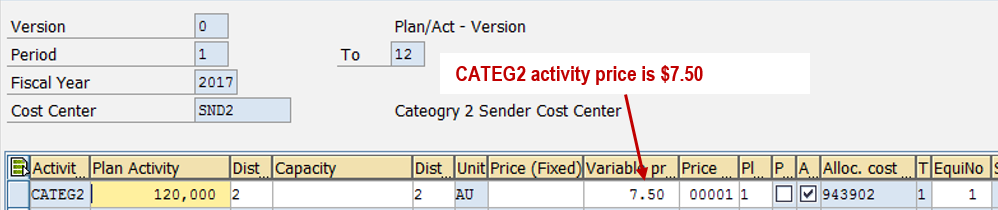

In our example, planning for this activity type is performed using the same method we used for the category 1 activity. This is because we used planning category 1 when we created CATEG2 as shown in Figure 1. You plan activity quantity with transaction KP26, and assign costs with transaction KP06. You calculate the activity price with transaction KSPI. In our example, we are planning $900,000 in variable costs for cost element 550000 for CATEG2 in cost center SND2. The resulting activity price is $7.50 per activity unit as shown in Figure 2.

Figure 2 Plan Activity Prices With Transaction KP26

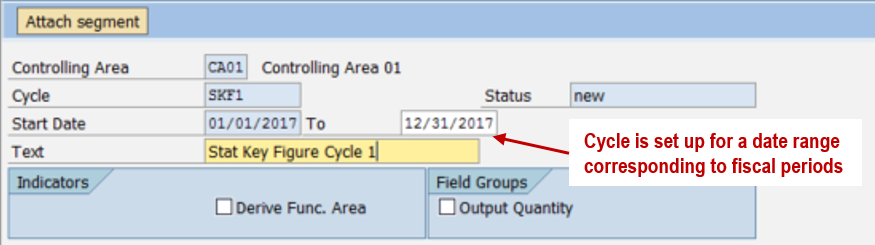

In order to post category 2 activities, you must create an indirect activity allocation cycle with transaction KSC1 as shown in Figure 3. The indirect activity allocation cycle defines rules for calculating the activity quantity that is posted and also defines the receivers that are used for those activity postings. Once you create the cycle, it can be reused throughout the fiscal year to process multiple activity postings at a time without having to manually determine the quantities to post to each receiver. Let's look at two examples.

In our first example we'll use statistical key figure postings in the receiver cost centers to calculate the quantity of activity to post from the sender. The transactions for maintaining actual indirect activity allocation cycles are KSC1 (create), KSC2 (modify), KSC3 (view), and KSC4 (delete) as shown in Figure 3. You run cycles for a fiscal period.

Figure 3 Change Actual Indirect Activity Alloocation Cycle Header Data Transaction KSC2

Cycles are made up of segments. Click the Attach segment button shown in Figure 3 to define a segment as shown in Figure 4. Each segment defines a separate allocation method for different senders and receivers.

Figure 4 Define Cycle Segment

The Segment Header tab defines how the sender values are determined and what receiver types will be used to determine the quantities to be posted. Three rules are supported for senders: Posted Quantities, Fixed Quantities, and Quantities Calculated Inversely.

Posted Quantities means that the sender activity type must first have a quantity posted and then the allocation is based on the receiver definitions. We'll discuss this in detail in the category 3 activity type.

Fixed Quantities means that the quantities to be posted are maintained directly in the cycle and then allocated based on the receiver definitions. This requires cycle maintenance each time the cycle is run.

Quantities Calculated Inversely, you would normally use for category 2 activity type postings. The quantity of activity is calculated from postings made at the receiver cost object, and this is the rule we will discuss.

The four receiver allocation rules are: Variable Portions, Fixed Amounts, Fixed Percentages, and Fixed Portions.

Variable Portions: The sender activity quantity to be allocated to the receiver cost object is calculated by the weighting factor times the quantity of the tracing factor that is posted. The tracing factor could be a specific statistical key figure or activity type that is posted to the receiver cost object. For example, if we used a statistical key figure as our tracing factor, then the quantity of sender activity allocated to the receiver would be the statistical key figure amount times the weighting factor. For example, if there were 15 units of a statistical key figure posted to cost center B with a weighting factor of 5, then that would equate to 75 units of activity type posted to cost center A with the costs allocated to B. The quantities allocated to all the receivers defined in the segment would then be added together and that would be the total of activity units posted in the sender cost center.

Variable Portion Type define which type of posting will be used to calculate the allocations. These can be actual or planned costs by cost element, actual or planned consumption, actual or planned statistical key figure postings, actual or planned activity type postings, or actual or planned statistical costs. In this first example we'll use actual statistical key figure postings.

The scaling option determines how negative postings will be treated in the calculation of the activity allocations. For the sake of simplicity (!), we will assume that there will be no negative postings, and therefore, no scaling is required.

The Senders/Receivers tab is used to define the sender cost center/activity type and the receiver cost objects. My examples will always assume that the receivers are cost centers.

Figure 5 Segment Senders/Receivers Tab

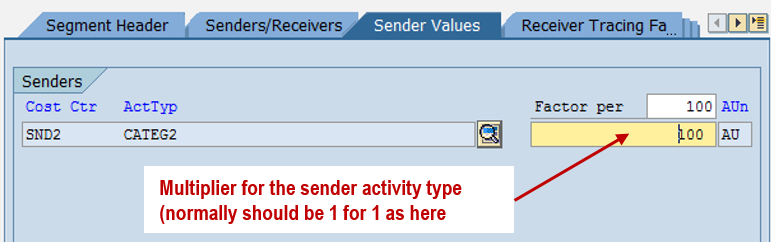

The Sender Values tab shown in Figure 6 is used to adjust the quantity of sender that is calculated. In normal circumstances this should be left as 1 to 1.

Figure 6 Segment Sender Values Tab

You define the actual tracing factor used on the Receiver Tracing Factor tab as shown in Figure 7. Since the cycle has selected Actual Statistical Key Figures as the variable portion type, you need to define a specific statistical key figure or set of statistical key figures.

Figure 7 Segment Receiver Tracing Factor Tab

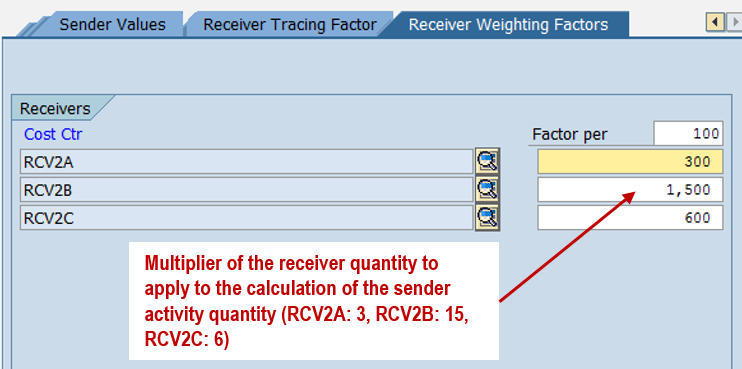

Finally, the Receiver Weighting Factors tab shown in Figure 8 is used to define the multiplier that will be applied to the quantity of “tracing factor” posted to calculate the quantity of activity to be posted to the sender for allocation to each receiver.

Figure 8 Segment Receiver Weighting Factors Tab

You can add additional segments to the cycle at this time to cover other types of allocations.

Since we have set this cycle to use statistical key figures posted at the receivers to determine our sender postings and allocations, we need to use KB31N to post the statistical key figures as shown in Figure 9.

Figure 9 Post Statistical Key Figures

Now, let’s look at the Cost Center Actual/Target/Variance report prior to running the allocation cycle. As you can see in Figure 10, there are no actual costs or activities posted in cost center SND2.

Figure 10 Cost Center SND2 Report

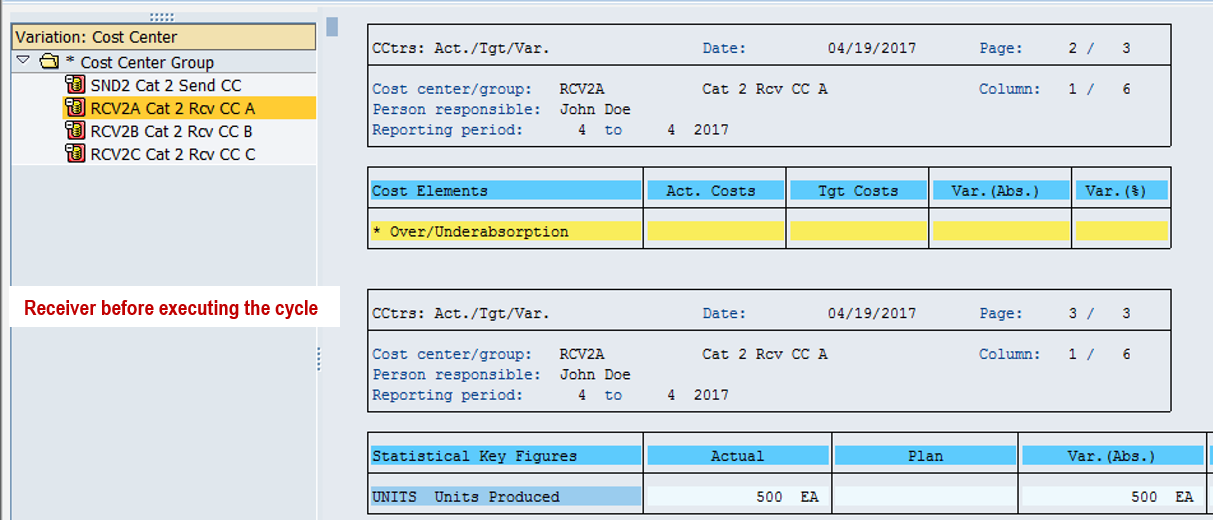

You also see that in cost center RCV2A shown in Figure 11, 500 Units Produced have posted, but again no actual costs are posted.

Figure 11 Cost Center RCV2A Report

RCV2B also has 500 Units Produced posted but no costs.

Cost center RCV2C has 1000 Units Produced posted.

Now, let’s run transaction KSC5 to execute the indirect activity allocation cycle. We'll run it for period 4 (April), with cycle SKF1 for fiscal year 2017 as shown in Figure 12.

Figure 12 Execute Indirect Activity Allocation Cycle

A report is generated when you run the cycle which will show the results of the postings as shown in Figure 13. The result is that a total of 15,000 units of CATEG2 was posted from cost center SND2 and allocated to three receiver cost centers: 1,500 to RCV2A, 7,500 to RCV2B, and 6,000 to RCV2C.

Figure 13 Allocation Cycle Report

Looking at the cost center report for the four cost centers, we can see these postings. How did the cycle determine that these were the quantities to be posted? Since the receiver rule was set to Variable Portions, the calculation was based on the receiver quantities posting along with the weighting factors. The quantity calculation is (500 x 3) + (500 x 15) + (1,000 x 6) = 15,000. We see posted in cost center SND2 as shown in Figure 14.

Figure 14 Cost Center SND2 Report

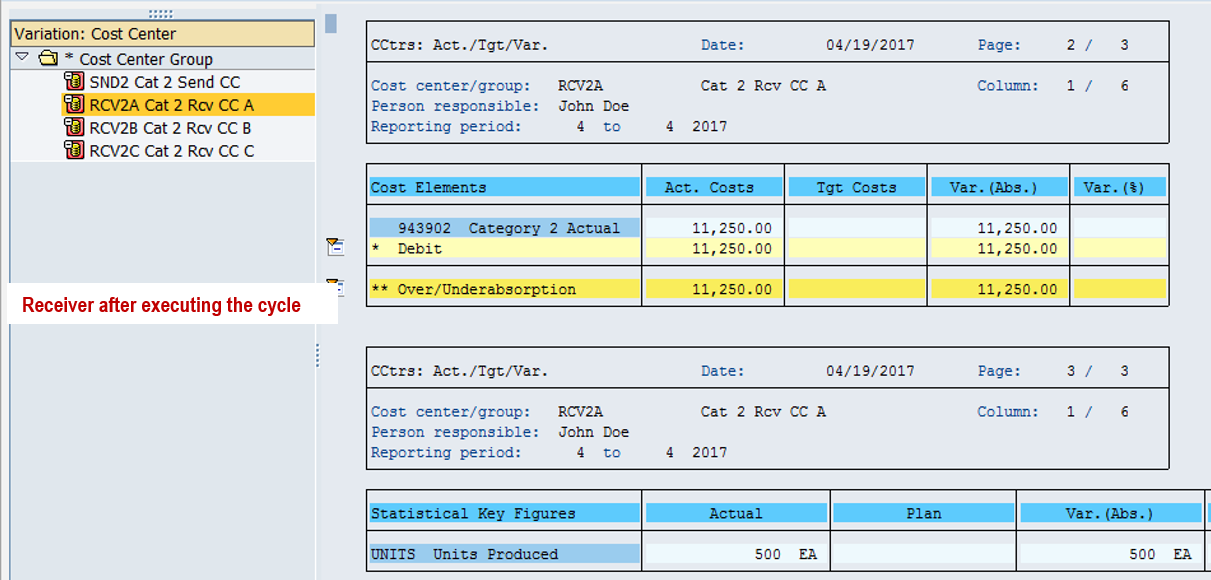

Note that cost centers RCV2A and RCV2B both had 500 Units Produced posted, but the amounts posted to each are different. That is because the weighting factor in the cycle was different for each cost center. Cost center RCV2A had a weighting factor of 3, which translates to 1,500 activity units posted in SND2 with RCV2A as the receiver as shown in Figure 15. If we think of our statistical key figure as representing units of production, and CATEG2 as representing energy consumption, that would mean it would take 3 units of energy consumption to make each production unit. The value posted for cost element 943902 is then CATEG2 price of $7.50 times 1,500 or $11,250.

Figure 15 Cost Center RCV2A Report

Using our energy analogy from cost center RCV2A, the expected energy consumption for each production unit in RCV2B is 15. The weighting factor in the cycle represents this. Consequently, 7,500 units of CATEG2 were posted in SND2 and allocated to RCV2B, resulting in $56,250 posted to 943902 as shown in Figure 16.

Figure 16 Cost Center RCV2B Report

To round out the receiving cost centers, 1,000 units of production with a weighting factor of 6 results in 6,000 units of CATEG2 being posted as shown in Figure 17.

Figure 17 Cost Center RCV2C Report

The cycle as defined can be used again and again to calculate the activity quantities to be posted each fiscal period. All that is needed is that the statistical key figures be posted for the receiver cost centers each period.

The second example how the indirect activity allocation cycle works is shown in the next blog post. It will cover using receiver activity types as the method for calculating and allocating the sender quantities.

![]() Tom King recently retired from Milliken, a leading global manufacturer of specialty textiles, floor covering, and chemicals based in Spartanburg, South Carolina. He was lead SAP CO analyst and has more than 30 years of experience in manufacturing and product costing. Tom has published three SAP books with Espresso Tutorials:

Tom King recently retired from Milliken, a leading global manufacturer of specialty textiles, floor covering, and chemicals based in Spartanburg, South Carolina. He was lead SAP CO analyst and has more than 30 years of experience in manufacturing and product costing. Tom has published three SAP books with Espresso Tutorials:

- Practical Guide to SAP CO Templates

- SAP S/4HANA Product Cost Planning Configuration and Master Data

- SAP S/4HANA Product Cost Planning Costing with Quantity Structure

Comments 1

very nice