By Janet Salmon

Table of Contents

- Inventory Accounting

- Universal Parallel Accounting & Product Costing

- Unconsolidated Views

- Consolidated View

- Ledgers in Universal Parallel Accounting

- Parallel Currencies for Product Costing

- Currency Settings for Group Valuation Ledger

- Material Valuation

- Standard Cost Estimates

- Actual Costing

- Bal Sheet Valuation

- Comments

- Glossary

Inventory Accounting

Let's look at Universal Parallel Accounting UPA in SAP S/4HANA 2022 about Inventory Accounting and explain the changes in:

- Material Valuation

- Product Cost Planning

- Actual Costing

- Balance Sheet Valuation

Universal Parallel Accounting & Product Costing

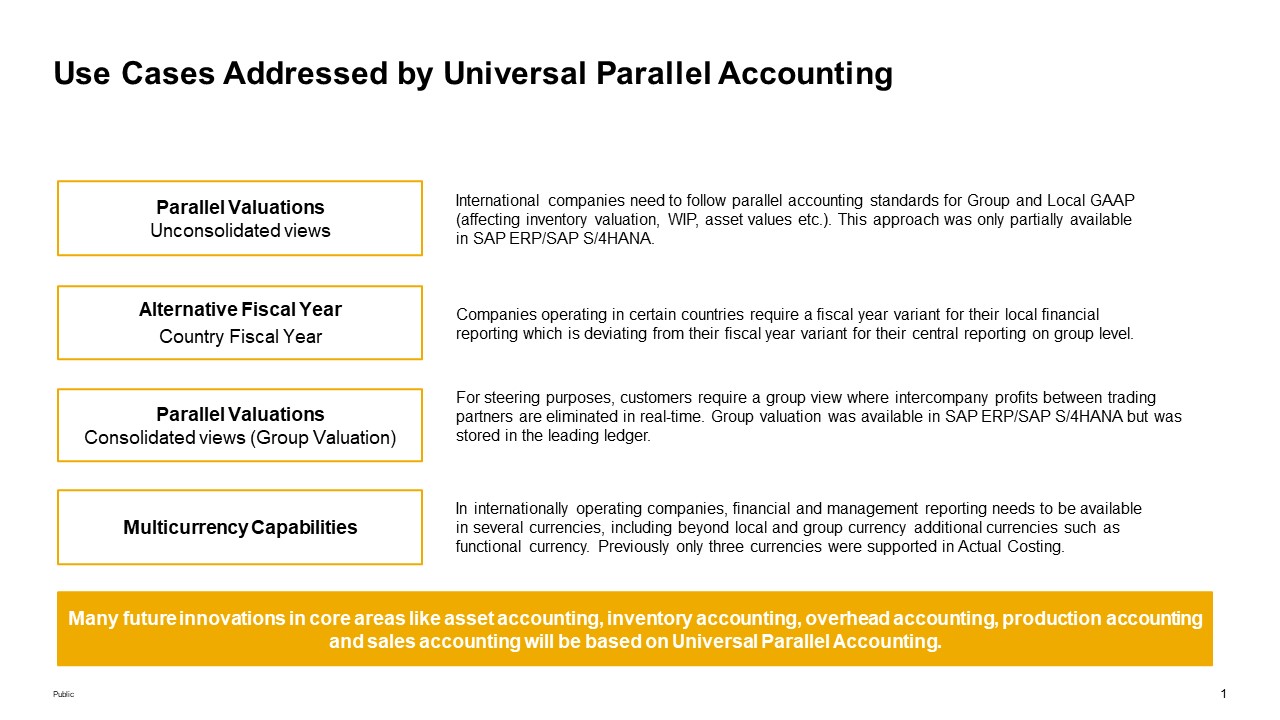

UPA offers two types of parallel valuations for product costing: unconsolidated views, which represent different legal valuations, and a consolidated view, which is a group valuation. The differences are illustrated in the four UPA Use Cases in Figure 1.

Figure 1: Universal Parallel Accounting Use Cases

Unconsolidated Views

Based on corporate and local accounting principles, the unconsolidated views focus on valuing materials differently. Typically, one common accounting principle (such as IFRS) is used in all countries, alongside many different accounting principles based on local GAAPs in various countries. Also, some countries, such as Brazil, require Actual Costing. You may be familiar with this approach if you've worked with the business function Parallel Cost of Goods Manufactured FIN_CO_COGM.

The new approach is more comprehensive as it enables you to carry the same material with multiple legal prices and standard costs and to calculate production variances and contribution margins in each ledger. This provides an end-to-end view of product profitability that can vary depending on the underlying accounting principles.

Consolidated View

With the consolidated view, the focus is on achieving a group view for intercompany value flows, distinct from transfer prices used by affiliated companies as they trade among one another at arm's length. This approach, known as group valuation, differs from legal valuation because it excludes transfer pricing.

With UPA, we introduce a consolidation-like approach in which the intercompany revenues and Cost of Goods Sold COGS are eliminated in a separate ledger whenever an intercompany boundary is crossed within the group, such as when a manufacturing company sells to distribution center or the distribution center sells to the selling company who manages the business with the final customer. The at-cost valuation continues to be supported for the valuation of intercompany goods movements, ensuring that profit in inventory is excluded in the group view. Profit center valuation is not yet available with UPA, but it is planned for release in Q2023.

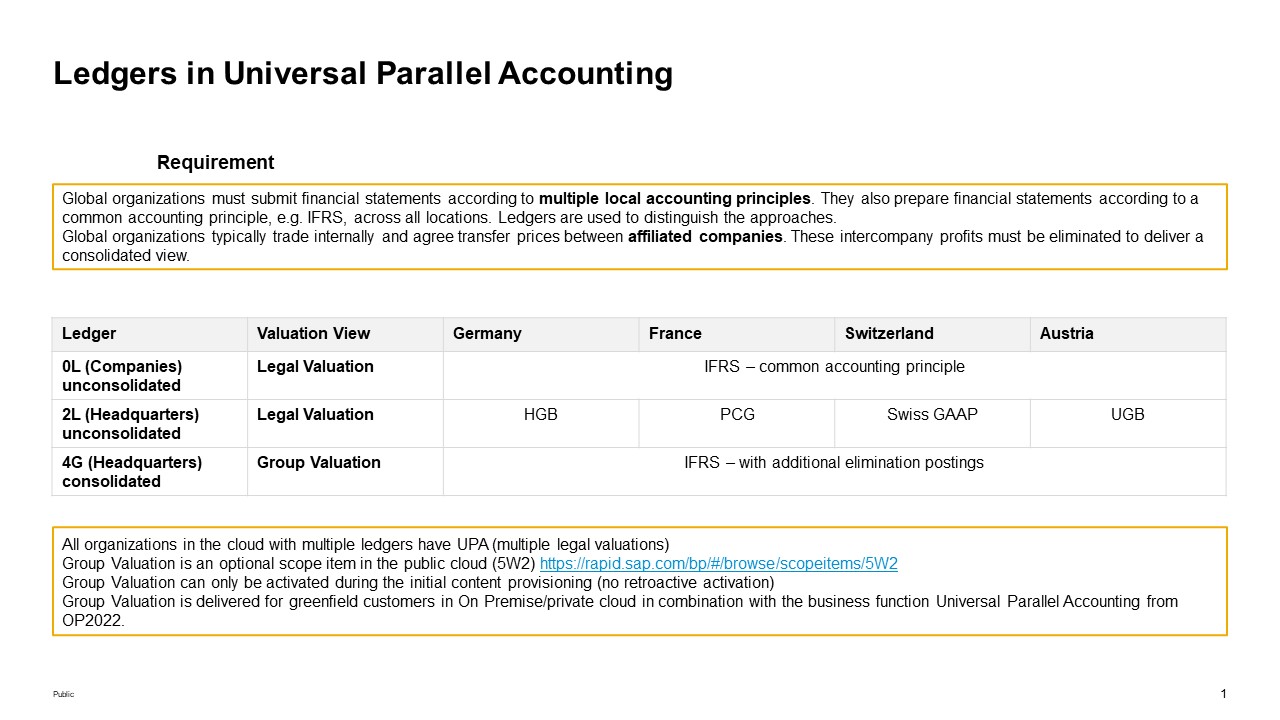

Customers who used group and profit center valuation in the past stored these additional valuation views in the leading ledger (multi-valuation ledger). The new approach is based on single valuation ledgers, where the unconsolidated views are separated by ledger (as before), and an additional single valuation ledger is enabled for group valuation. Figure 2 provides a schematic view of the new approach, showing two unconsolidated views (or legal valuations) in ledgers 0L and 2L and one consolidated view (or group valuation) in ledger 4G.

If you are not using UPA, the previous multi-valuation ledger recommendation still applies (see SAP Note: Implementing Transfer Prices). However, with UPA, the new ledger for group valuation uses the same accounting principle and fiscal year variant as ledger 0L (previously, Asset Accounting did not support using the same principle in multiple ledgers). The ledger settings are delivered as best practice business content. Since UPA is only available for greenfield customers, you may find it helpful to use this content during the initial setup of your system. It is also not possible to add additional ledgers once accounting entries have been made in the Universal Journal.

Figure 2 Ledgers in Universal Parallel Accounting

Parallel Currencies for Product Costing

While the need for parallel valuations is likely to drive initial discussions in this area, the other topic of interest for many customers is the ability to use multiple currencies in parallel (see Figure 1). Actual Costing historically supported three currencies, and if you worked with group valuation then currency type 31 (group valuation in group currency) occupied one of the currency columns in the multi-valuation ledger, alongside the column for company code currency and group currency, meaning that international organizations would run out of currencies if they required a different functional currency or an index currency in some countries. The universal journal has supported using ten currencies since SAP S/4HANA OP1610. Still, it's now possible to have up to ten currencies in Actual Costing, allowing you to have a local currency, a group currency, a functional currency, and any other currency needed in the legal ledger and the group valuation currencies in the group ledger. This approach handles all currencies consistently in the actual costing run at the period's close.

In SAP ERP, the currency and valuation profile determined whether the leading currency for group valuation was the controlling area currency (currency type 31) or the local currency (currency type 11).

The leading currency was used to determine which currency would value the intercompany goods transfer in combination with the price condition KW00. The other currency will be filled using a conversion at the time of posting.

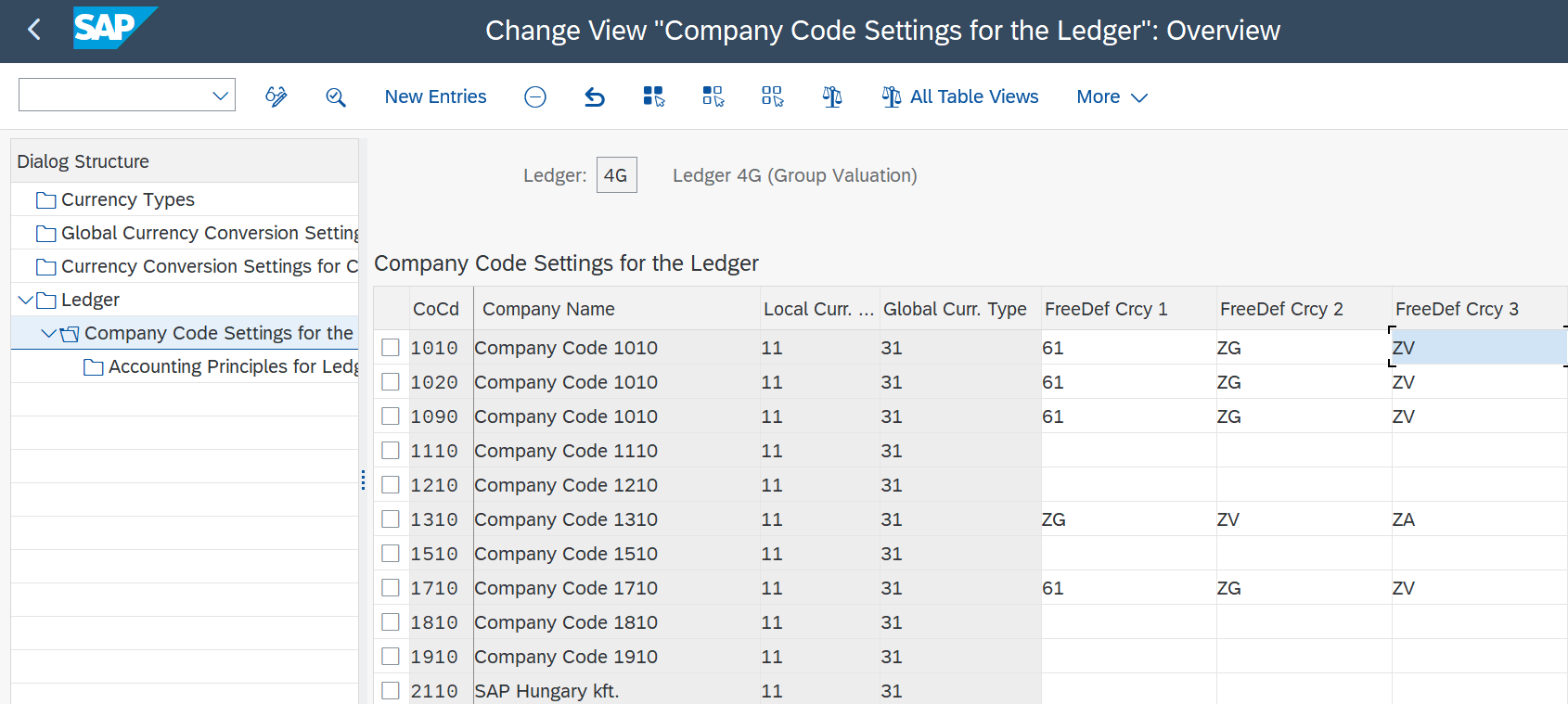

The new approach defines the currencies used in the group ledger via the ledger settings, and the currency and valuation profile become obsolete with UPA. Figure 3 shows a sample ledger for group valuation with currency types 11 (local currency) and 31 (group currency) and various additional currencies. The new approach treats all currencies equally, allowing you to have a consistent group view in multiple currencies. In other words, an intercompany goods movement will be valued using all currencies active in the group valuation ledger, rather than converting from the leading currency. Note that currency type 20 is no longer supported.

Figure 3 Currency Settings for Group Valuation Ledger

Material Valuation

Let's discuss the different types of prices available in SAP S/4HANA. Since the material ledger is automatically active, you can manage a different material price for the same material (group price and legal price). You can also enter different planned, commercial, or tax prices for the same material. Still, it is not possible to have different legal prices for the same material without UPA.

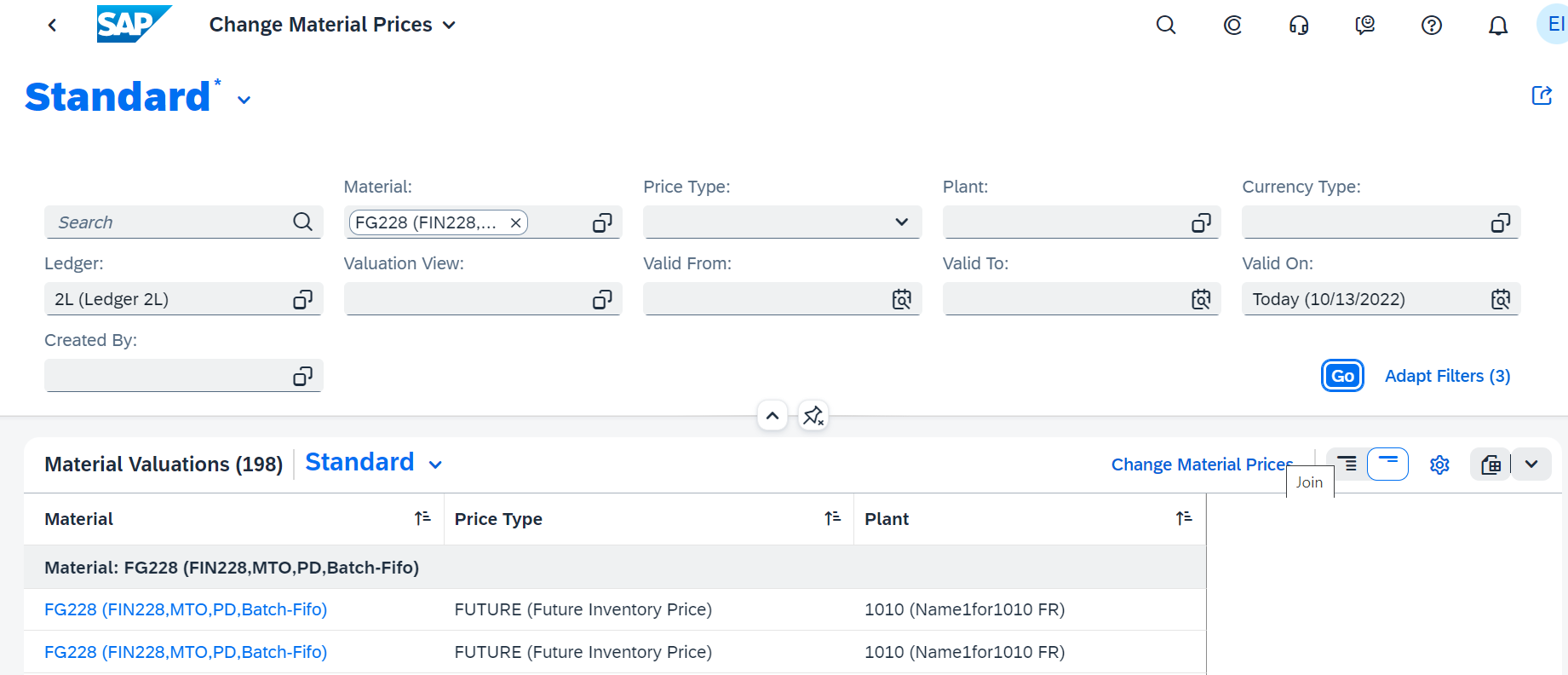

With the activation of UPA, you can use different material prices as the initial valuation of the goods movements in each ledger and to provide a basis for variance calculation in Production Accounting and the calculation of contribution margins in Margin Analysis. To support the link to the ledger and additional new functions, UPA requires the introduction of a new material price table, FMLT_PRICE. Figure 4 shows the new Change Material Prices app with the latest price types (STDPR, INVPR, FUTURE, and so on) and the selection by ledger (see header).

Figure 4 Change Material Prices app

The ability to manage ledger-specific material prices applies to both raw materials and trading goods, where the purchase price may be impacted by additional freight and duty costs, and finished goods, where the cost of goods manufactured may be affected by the different assumptions behind the asset values reflected in the activity prices and overhead rates.

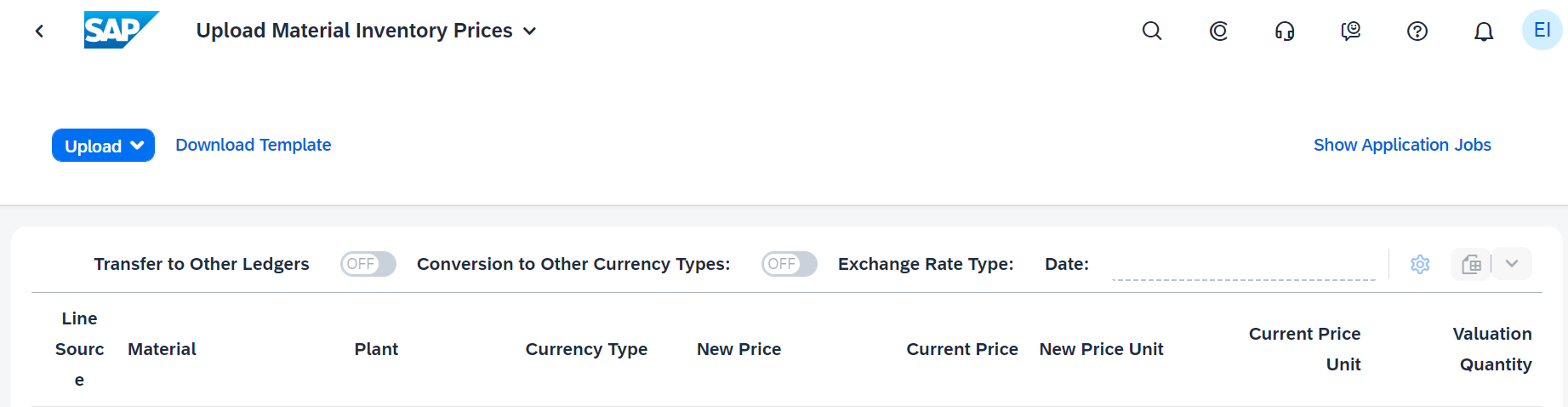

It is also possible to update using the material price update API and by Excel upload, as shown in Figure 5. You can update prices ledger-by-ledger or across all ledgers.

Figure 5: Upload Material Inventory Prices App

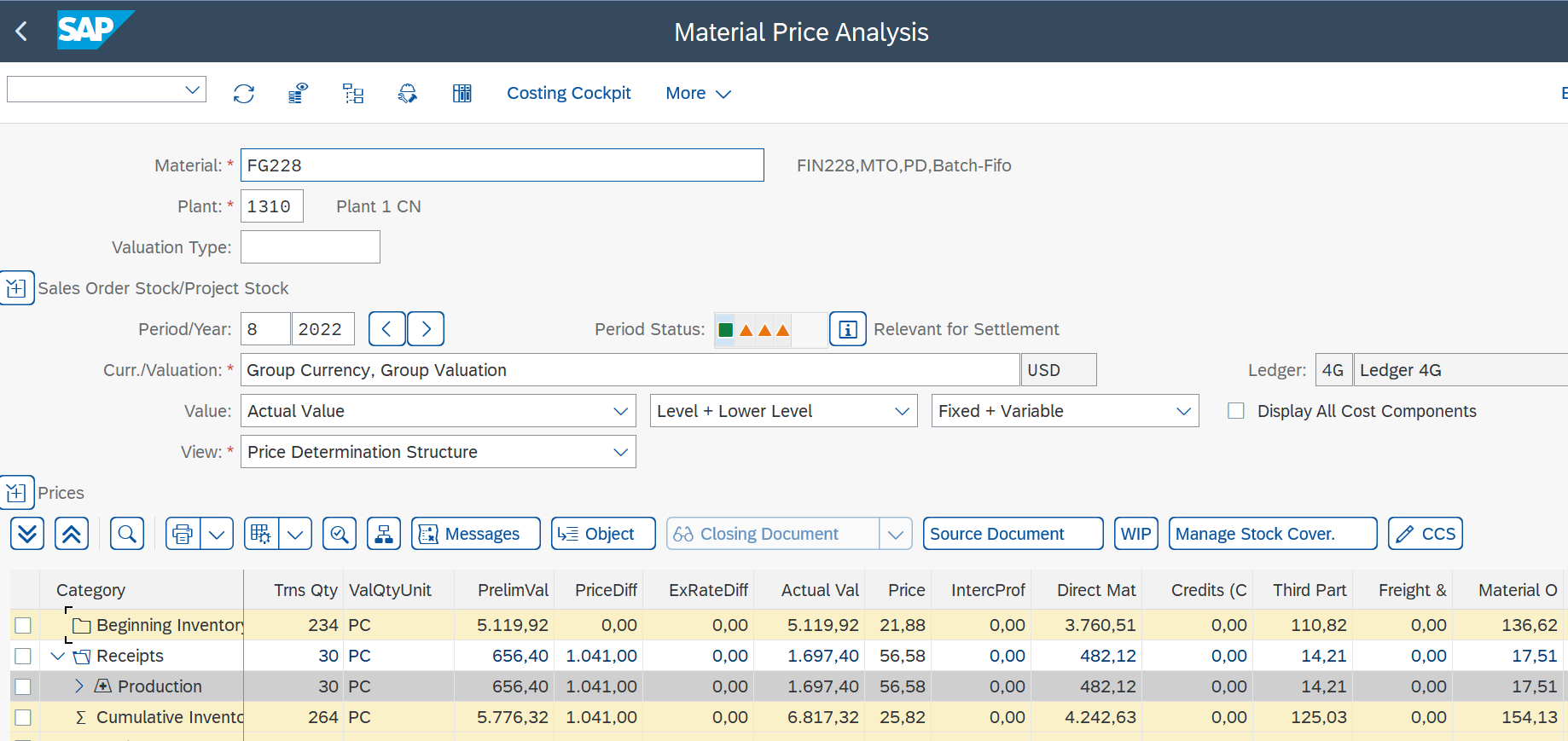

This variety is not yet reflected in all classic GUI transactions. If you use transactions MM01-3 to look at your material prices, you will only see the legal view in the leading ledger in the Accounting View. By contrast, Material Price Analysis (transaction CKM3N) shows all goods movements and settlements for the ledger. Figure 6 shows the goods movements and price changes for material FG228 in ledger 4G. You can use the Curr-/Valuation field to tab through the ledgers and the various currencies configured for these ledgers, allowing material price analysis in up to ten currencies.

Figure 6: Material Price Analysis (Transaction CKM3N) in Group Valuation Ledger

Standard Cost Estimates

Let's examine how to create the standard costs used for initial inventory valuation when goods movements are posted. Figure 7 illustrates the Manage Material Valuations app and its contents, specifically the Standard Cost Estimates tab. Here, we see that standard costs are also stored in a ledger. In the legal ledgers, two approaches are possible. You can either create one standard cost estimate using an existing costing variant that has no reference to a ledger and use it to update both legal ledgers or you can use the new costing variants, P00L which updates ledger 0L and P02L, which updates ledger 2L (or equivalent) if there are significant differences between the two accounting approaches. The cost estimate for group valuation continues to be a separate cost estimate because it supports a different valuation approach (the full BOM explosion is shown in the cost estimate, and the cost components are rolled up across all company codes as before). Still, now the costing type links the group cost estimate with the group valuation ledger (4G).

Figure 7: Current Material Valuation - Standard Cost Estimates

Creating multiple cost estimates for the same material is not new. Using various costing methods or variants, you can represent the assumptions underlying your cost estimate, such as standard costs and forecasts. What changes is the link to the ledger in the costing type, allowing you to update the material prices in the correct ledger when releasing the cost estimate. Figure 8 illustrates the existing costing variants (PPC1, PYC1, and PYC2 in this example), which update the same costs across multiple ledgers. The new costing variants feature different costing types per ledger (P00L, P02L, and P03L).

Figure 8: Sample Costing Variants

With UPA, you'll see the ledger in the costing and valuation data tabs of the standard cost estimate (transactions CK11N and CK13N) and the costing run (transaction CK40N). Note that this assignment means that you can treat the costing runs differently depending on the purpose of each ledger, performing local cost estimates and company code by company code, but creating group cost estimates with a worldwide costing run. Material cost estimates continue to be calculated and stored in the controlling area currency and object currency and are translated into the additional currencies defined for the ledger on release.

As well as creating separate cost estimates for each ledger, you'll need to mark and release (transaction CK24) the various cost estimates separately for each ledger, as shown in Figure 9, where we have linked the company code, the ledger, and the costing variant before releasing the cost estimates. Releasing a standard cost estimate results in revaluating any inventory on hand for that material and producing a journal entry for the revaluation. These standard cost estimates will be accessed to determine the ledger-specific variances on the production orders and the ledger-specific cost of goods sold for the deliveries to the customer. To learn more about how production variances are calculated in the new approach, please refer to Shuge Guo's blog: Production Accounting for Universal Parallel Accounting.

Figure 9: Marking and Releasing Cost Estimates (transaction CK24)

If you work in a make-to-order environment, the best practice scope item includes new costing variants for the costing of sales orders that follow the same basic principle. The difference is that all inventories are handled as valuated sales order stock, which can only be issued to the sales order that triggered the production process. Alternatively, you can manually create your own costing variants and link the costing types to your ledgers.

In an intercompany scenario, the revenues from the intercompany invoice and the cost of goods sold from the intercompany delivery will be posted in all ledgers (the cost of goods sold is ledger-dependent). In the legal ledger, the cost of goods sold is considered arm's length trading and recognized in the delivering company. However, an elimination posting in the group valuation ledger removes the intercompany cost of goods sold and posts to a valuation clearing account, as shown in Figure 10. Similarly, when the intercompany invoice is made from the delivering company to the selling company, the revenue is recognized in the legal ledger of the delivering company. Still, an additional elimination posting is made in the group valuation ledger that removes the intercompany revenue to a valuation clearing account.

Figure 10: Group Valuation with Elimination of Intercompany Business in Delivering Company

As the goods are moved from the delivering company to the selling company, the goods movement is valued with the group standard costs calculated using the group standard cost estimate and again stored in the group valuation ledger (4G), as shown in Figure 11. There is no elimination since the group standard costs used to value the goods movement do not include intercompany profit. This replaces the SAP ERP approach, where price condition KW00 was used to value the intercompany stock transfer with the group standard costs.

Figure 11: Group Valuation with At-Cost Valuation of Intercompany Goods Movement

This article does not fully describe the new options for intercompany sales and stock transfers. To learn more about the new approach, please read Gerhard Welker's blog, Advanced Intercompany Sales and Stock Transfer.

Actual Costing

If you work with Actual Costing, there are three scenarios to consider for UPA:

1. You only use Actual Costing in those locations that require it and thus need to perform a costing run only in those company codes where the local GAAP requires actual costs.

2. You are in an industry that uses Actual Costing in all locations and must create costing runs to cover all ledger/company code combinations.

3. You want to run Actual Costing with group valuation and thus need to ensure that actual costing is active in all company codes associated with the ledger.

The costing run CKMLCP is created using a run template (see Figure 12) that contains the link to the ledger and the associated company codes and determines whether the run applies to a single period or year-to-date. This choice will also affect Gerhard Welker period-by-period or cumulatively over the year.

Since the templates are ledger-specific, you might only create one for those countries requiring actual costing according to their local GAAP or for all ledgers. The entries in the Company Code Assignment tab will ensure that the costing run covers all plants in the selected company code (it is not possible to deselect plants in a company code). Since the costing run can be run separately for each ledger, you can perform the group valuation run independently of the legal run(s).

Figure 12: Template for Costing Run

The costing run shown in Figure 13 references the run template to determine the relevant ledger, company code(s), and whether the costs apply to a single or year-to-date period. As we saw in Product Cost Planning, you will calculate actual costs and update the inventory and cost of goods sold values for each ledger separately. If you perform a costing run for the purposes of group valuation, the ledger includes all company codes in the controlling area, and you'll need to set up the costing run to include all plants in those company codes.

Note that you will no longer need to work with a separate alternative valuation run to deliver a different legal valuation or cumulate local periodic runs for group valuation or year-to-date calculations since the ledger alone determines the purpose and scope of the costing run. Each costing run is independent of the others.

Figure 13: Ledger-Specific Costing Run for Actual Costing

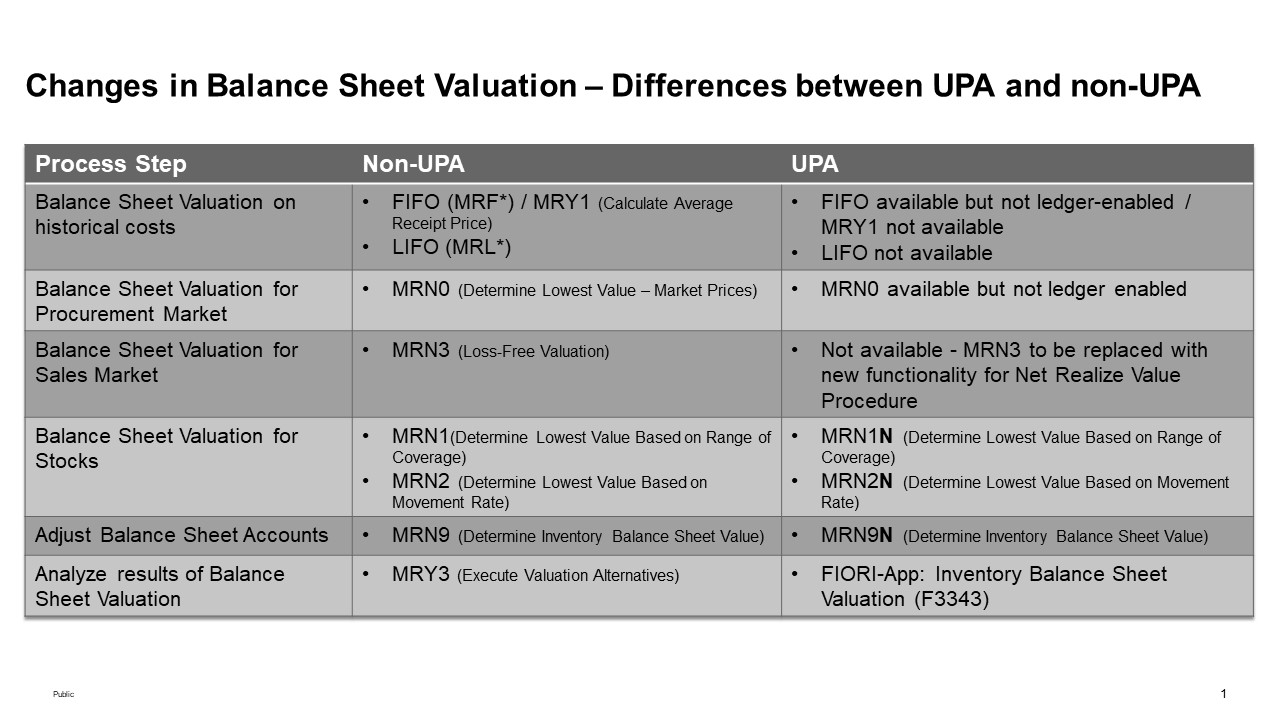

Balance Sheet Valuation

Figure 14 provides an overview of the balance sheet valuation functions supported in the past and combined with Universal Parallel Accounting. The balance sheet valuation programs do not support group valuation.

Figure 14: Balance Sheet Valuation Methods

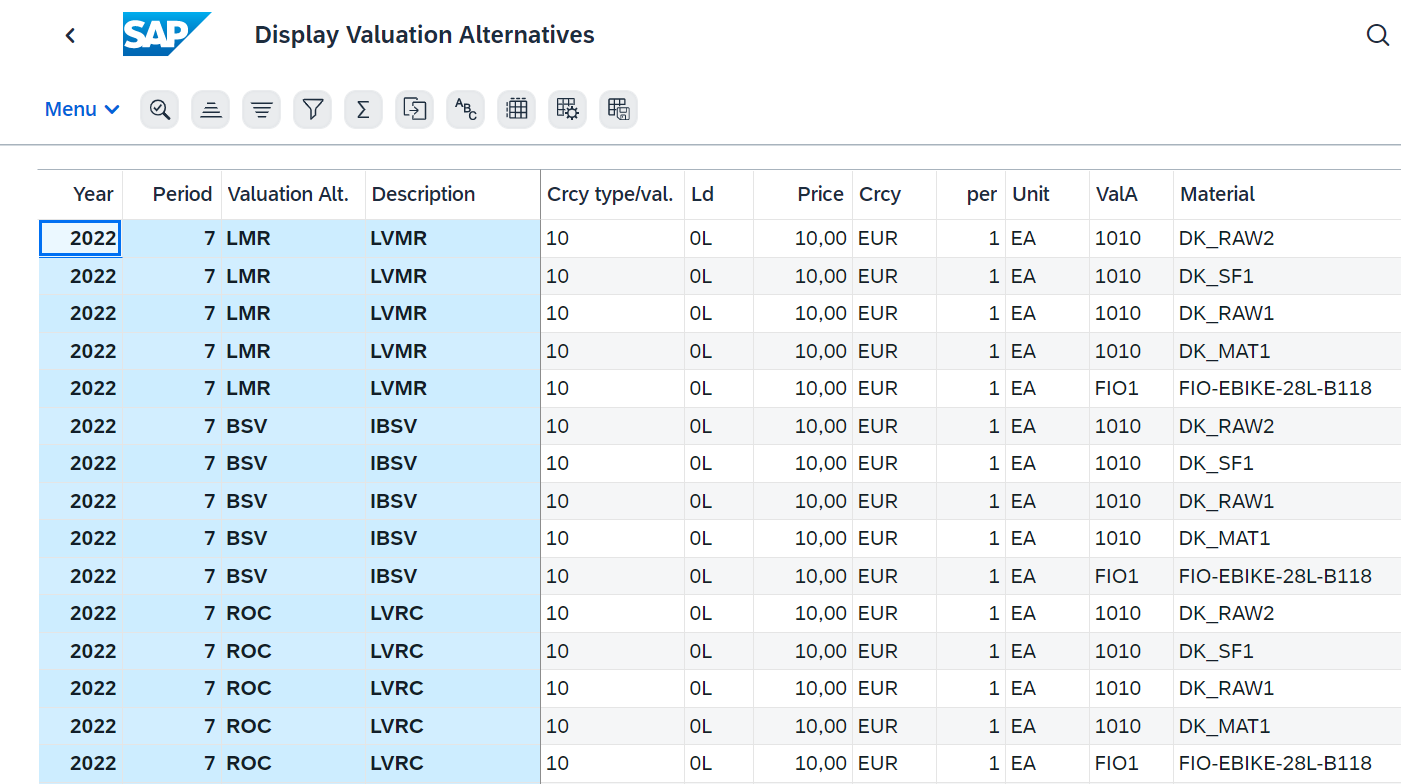

With UPA, the tax and commercial prices in the material master are removed. The various balance sheet options are represented as valuation alternatives, as shown in Figure 15. Here, we see the methods (lowest value by market price (LVMP), lowest value by movement rate (LVMR), inventory balance sheet value (IBSV), lowest value by range of coverage (LVRC), and so on) and the link between the valuation alternative and the ledger.

Figure 15: Valuation Alternatives app

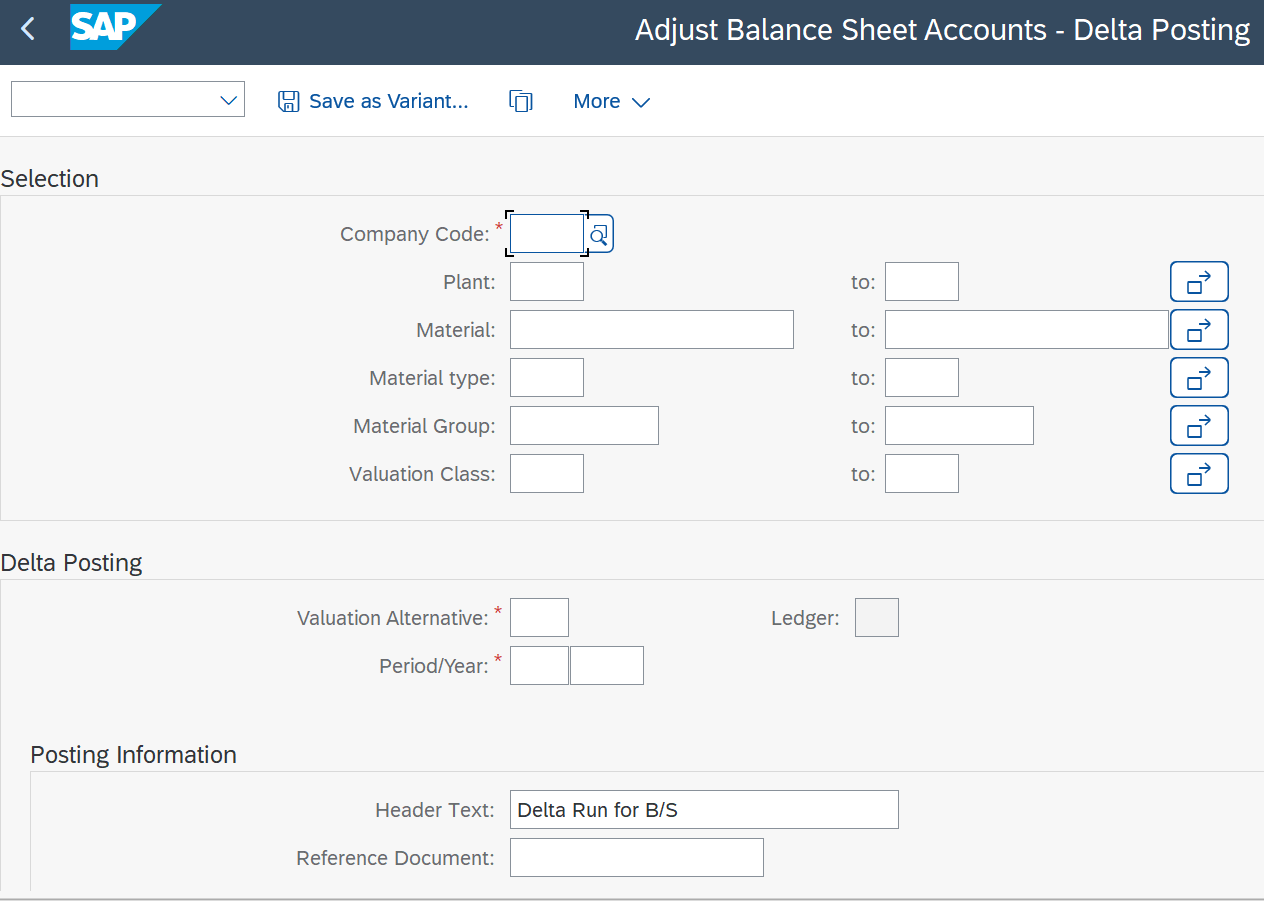

The ledger is included in the Adjust Balance Sheet Accounts - Delta Posting app (transaction MRN9N). The results of the various calculations are used to make balance sheet adjustments at year-end, as shown in Figure 16.

Figure 16: Adjust Balance Sheet Accounts

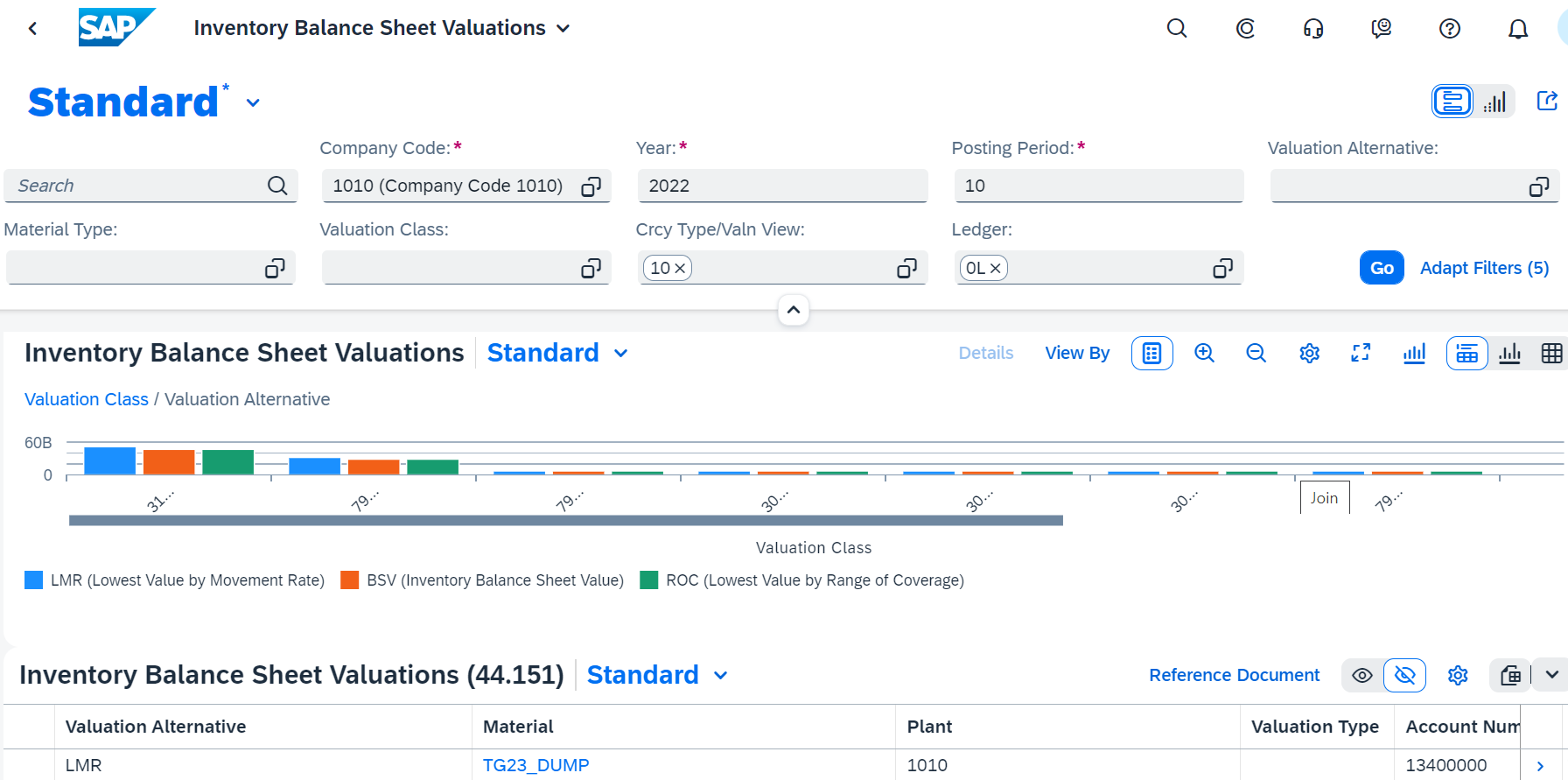

Finally, the balance sheet valuation results can be displayed in the Inventory Balance Sheet Valuations app, as shown in Figure 17. Notice the fields Valuation Alternative and Ledger in the selection screen.

Figure 17: Inventory Balance Sheet Valuations app

Comments

This approach simplifies a company's ability to handle the requirements of different accounting principles in inventory management. It removes the need for manual work to reflect the different approaches to dealing with varying material prices, standard costs, actual costs, and balance sheet requirements.

Since this is the first release of UPA, it is important to compare the delivered scope with that required for your project. Functions that aren't supported are unavailable in the SAP Easy Menu if the business function for universal parallel accounting is active. This means you won't find transactions to create material cost estimates without quantity structure or alternative valuation runs in such systems.

Universal Parallel Accounting is activated using a business function. For more details, please refer to the documentation: Business Function: UPA

For a complete list of restrictions, refer to SAP Note 3191636: Universal Parallel Accounting - Scope Information.

This blog coincides with the release of SAP S/4HANA OP2022. This approach was introduced earlier in the cloud, and I described its impact on legal valuation in my previous blog: Inventory Accounting for Universal Parallel Accounting in SAP S/4HANA Cloud 2105. The functions for group valuation described here will be offered to greenfield cloud customers in CE2308 via the scope item 5W2.

Join us at the SAP Controlling conference to learn more about SAP GRIR and other S/4HANA topics.

Click Here for Conference Details

Glossary

Automatic Account Assignment

Automatic account assignment allows you to enter a default cost center per cost element within a plant with Transaction OKB9.

Backflushing

Backflushing is the automatic posting of a goods issue for components after their actual physical issue for use in an order. The goods issue posting of backflushed components is carried out automatically during confirmation.

Backflushing reduces the amount of work in warehouse management, especially for low-value parts. The material components from the BOM required in the operation should be assigned to the operations in the routing.

Cost Estimate

A cost estimate calculates the plan cost to manufacture a product or purchase a component. It determines material costs by multiplying BOM quantities by the standard price, labor costs by multiplying operation standard quantities by the plan activity price, and overhead values by the costing sheet configuration.

Costing Lot Size

The costing lot size in the Costing 1 view determines the quantity on which the cost estimate calculations are based. To reduce lot size variance, the costing lot size should be set as close as possible to actual purchase and production quantities.

Goods Issue

A goods issue is the movement (removal) of goods or materials from inventory to manufacturing or to a customer. When goods are issued, it reduces the number of stock in the warehouse.

Goods Receipt

It is a goods movement used to post goods received from external vendors or from in-plant production. All goods receipts increase stock in the warehouse.

Internal Order

An internal order monitors an organization's costs and revenue for short—to medium-term jobs. Planning can be carried out at a cost element and detailed level, and budgeting can be carried out at an overall level with availability control.

Profit Center

A profit center receives postings parallel to cost centers and other master data, such as orders. Profit Center Accounting (PCA) is a separate ledger that enables reporting from a profit center's point of view. Profit centers are usually created based on areas in a company that generate revenue and have a responsible manager assigned.

If PCA is active, you will receive a warning message if you do not specify a profit center, and all unassigned postings are made to a dummy profit center. You activate profit center accounting with configuration Transaction OKKP, which maintains the controlling area.

Purchasing Info Record

A purchasing information record stores all information relevant to procuring a material from a supplier. It contains the Purchase Price field, which the standard cost estimate searches for when determining the purchase price.

Scheduling Agreement

A scheduling agreement is a longer-term purchase arrangement with a vendor that covers the supply of materials according to predetermined conditions. These conditions apply for a predefined period and a total purchase quantity.

Standard Hierarchy

A standard hierarchy represents your company structure. A standard hierarchy is guaranteed to contain all cost centers or profit centers because a mandatory field in the cost and profit center master data is a standard hierarchy node.

Standard Price

If price control is set at standard (S), the standard price in the Costing 2 view determines the inventory valuation price. The standard price is updated when a standard cost estimate is released. You normally value manufactured goods at the standard price.

Surcharge

When calculating a project's lifecycle costs, you can apply surcharges to material and activity prices to account for increases or decreases in item prices over time.

Target Costs

Target costs are plan costs adjusted by the delivered quantity. For example, if the quantity delivered to inventory is 50% of the planned quantity, target costs are calculated as 50% of the planned costs.

Material Master

A material master contains all of the information required to manage a material. Information is stored in views, each corresponding to a department or area of business responsibility. Views conveniently group information together for users in different departments, such as sales and purchasing.

Origin Group

An origin group separately identifies materials assigned to the same cost element, allowing them to be transferred to separate cost components. The origin group can also determine the calculation base for overhead in costing sheets.

Price Control

The Price control field in the Costing 2 view determines whether inventory is valuated at standard or moving average price.

Price Unit

The price unit is the number of units to which the price refers. Increasing the price unit can increase its accuracy. To determine the unit price, divide the price by the price unit.

Process Order

Process orders are used to produce materials or provide services in a certain quantity and on a specific date. They allow resource planning, process order management control, account assignment, and order settlement rules to be specified.

Procurement Alternative

A procurement alternative represents one of several different ways of procuring a material. You can control the level of detail in which the procurement alternatives are expressed through the controlling level. Depending on the processing category, there are single-level and multilevel procurement alternatives. For example, a purchase order is single-level procurement, while production is multilevel.

Production Order

For discrete manufacturing, a production order is used. A BOM and routing are copied from master data to the order. The routing supplies a sequence of operations, which describes how to carry out work steps.

An operation can refer to a work center where it is to be performed. It contains planned activities required to carry out the operation. Costs are based on the material components and activity price multiplied by a standard value.

Product Drilldown Reports

Product drilldown reports allow you to slice and dice data based on characteristics such as product group, material, plant, cost component, and period. Product drilldown reports are based on predefined summarization levels and are relatively simple to set up and run.

Production Variance

Production variance is a calculation based on the difference between net actual costs debited to the order and target costs based on the preliminary cost estimate and quantity delivered to inventory. You calculate production variance with the target cost version 1. Production variances are for information only and are not relevant for settlement.

Production Version

A production version determines which alternative BOM is used and which task list/master recipe to produce a material or create a master production schedule. You can have several production versions for one material for various validity periods and lot-size ranges.

Purchase Price Variance

When raw materials are valued at the standard price, a purchase price variance will appear during the goods receipt if the goods receipt or invoice price differs from the material standard price.

Profitability Analysis

Costing-based profitability analysis enables you to evaluate market segments, which can be classified according to products, customers, orders (or any combination), or strategic business units, such as sales organizations or business areas concerning your company's profit or contribution margin.

Profit Center

SAP Profit Center is a management-oriented organizational unit used for internal controlling purposes. Segmenting a company into profit centers allows us to analyze and delegate responsibility to decentralized units.

Purchasing Info Record

A purchasing information record stores all the information relevant to procuring a material from a supplier. It contains the Purchase Price field, which the standard cost estimate searches for when determining the purchase price.

Raw Materials

Raw materials are always procured externally and then processed.