Welcome to the latest SAP S/4HANA edition of this groundbreaking SAP book. Our new edition, on publication, immediately entered and remains in the SAP Press Top Ten.

Table of Contents

- Introduction

- Chapter 1 Initial Planning

- Chapter 2 Cost Estimates

- Chapter 3 Actual Costs

- Chapter 4 Period-End Processing

- Chapter 5 Scrap Variance

- Chapter 6 Reporting

- Chapter 7 Future Direction of Variance Analysis

- Glossary

Introduction

The first edition, published in 2007, was the first-ever book on SAP Controlling (CO). It explains SAP CO in an Easy-to-Understand way and continues to attract enthusiastic positive feedback and comments from our SAP Controlling community.

The second edition, released in 2011, had a revised, improved layout and new content and continued as a best-seller.

To completely transform the book to the latest SAP S/4HANA version, Janet Salmon, Chief Product Owner of Management Accounting at SAP SE, co-authored with me. We've included the latest S/4HANA 2022 screenshots and content throughout the book.

Chapter 7 includes event-based processing, SAP Fiori Apps, and the future direction of SAP S/4HANA. It also includes new options for variance analysis delivered with SAP S/4HANA Cloud when you use scope item 3F0 (Event-Based Production Cost Posting) and SAP S/4HANA 2022, with the business function for universal parallel accounting.

Please find a comprehensive chapter-by-chapter review of this blog's updated contents and structure.

Pick up your copy here: Production Variance Analysis IN SAP S/4HANA

Chapter 1 Initial Planning

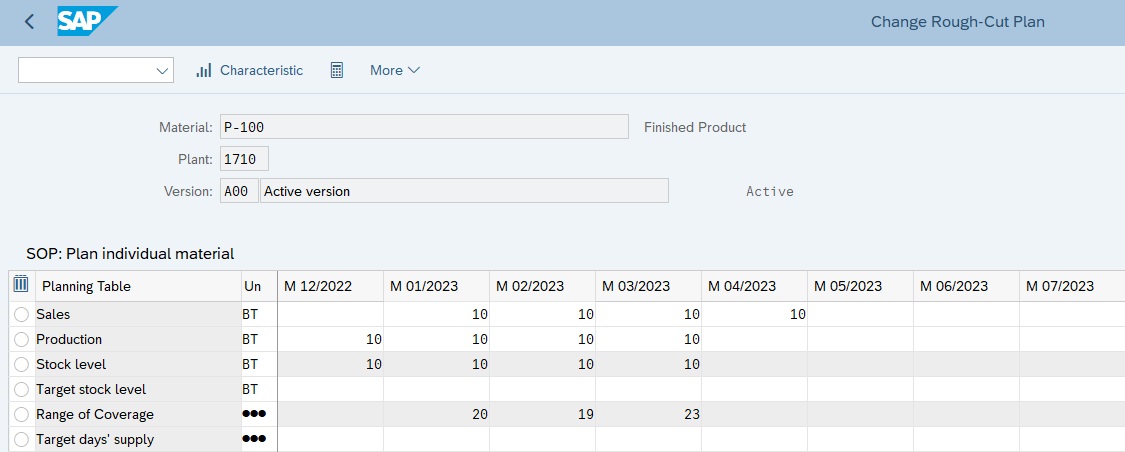

We provide an overview and details of the planning process with SAP Sales and Operations Planning and SAP Integrated Business Planning IBP to set the baseline for variance analysis.

Figure 1: Sales and Operations Planning

We examine sales and operations planning (S&OP), as shown in Figure 1. We also examine long-term planning to determine the raw materials to be purchased and the available manufacturing capacity to be reserved.

Note that S&OP is slowly being replaced by SAP Integrated Business Planning for Supply Chain (SAP IBP), which supports all S&OP features. S&OP is intended as a bridge or interim solution that allows a smooth transition from SAP ERP to on-premise SAP S/4HANA and SAP Integrated Business Planning IBP. See SAP Note 2268064 for details.

Note also that production versions are mandatory with SAP S/4HANA. They allow you to define which BOM alternative goes together with which routing alternative. They simplify MRP sourcing because there is only one option to determine the BOM and routing alternatives to manufacture a material. See SAP Note 2267880 for more details.

We look at cost center planning and how to combine the planned expenses and activity usage with setting the plan activity rates for activities.

Chapter 2 Cost Estimates

We introduce master data and explain the material master, BOM, routing, and work center to create cost estimates, as shown in Figure 2.

We present the role of the costing sheet in determining the overhead to be applied to your raw materials and manufacturing activities. We also discuss the configuration for the cost components and the costing variant.

Figure 2: Cost Estimate BOM and Routing

We then provide instructions for creating and releasing a cost estimate to set the standard price for a single material. We introduce the costing run to develop the standard costs for all materials in a plant. Where multiple production options exist for a material, we explain how to use a mixed cost estimate to combine different production or procurement alternatives to deliver one standard cost.

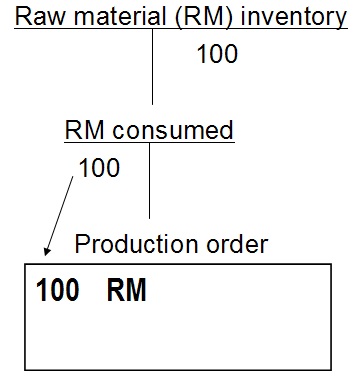

Chapter 3 Actual Costs

We introduce the Universal Journal and its impact on primary and secondary costs. We walk through the steps on the shop floor, such as production order and process order activity confirmation and component goods issues, that result in actual postings, as shown in Figure 3.

One of the fundamental changes in SAP S/4HANA is that the work center and operation are now part of the data structure for variance analysis.

Figure 3: Production Order Actual Costs During Goods Issue

We introduce two new critical SAP Fiori apps:

- Production Cost Analysis (ID F1780)

- Analyze Costs by Work Center and Operation (ID F3331)

Chapter 4 Period-End Processing

We explain how to configure SAP S/4HANA to calculate production variances and the variance categories to demonstrate their impact, including cost center and purchase price variance PPV.

We include detailed examples to help you easily understand period-end processing, including overhead, Work in Process WIP, variance calculation, and settlement.

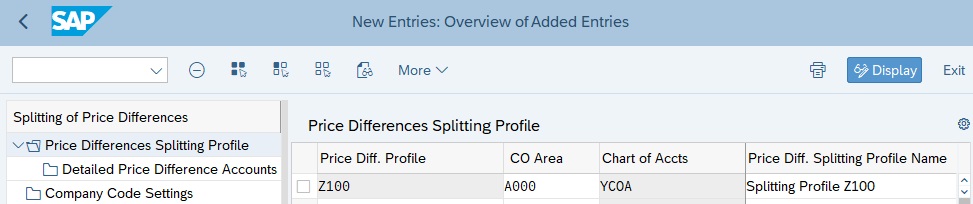

Figure 4: Variance Splitting Profile

We explain actual costing and how it rolls up purchase and production variances through the value chain as shown in Figure 4.

Chapter 5 Scrap Variance

We walk through the scrap calculation in detail, including:

- Assembly Scrap

- Component Scrap

- Operation Scrap

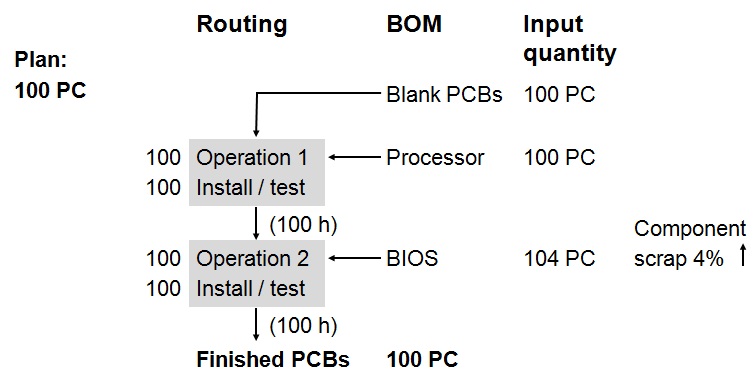

Figure 5: Component Scrap Increases Component Input Quantity

We explain the types of scrap, including Assembly Scrap, Component Scrap, and Operation Scrap, and their interaction as shown in Figure 5.

Chapter 6 Reporting

We explain the impact of production variances on product profitability and discuss the options for analyzing data in detail.

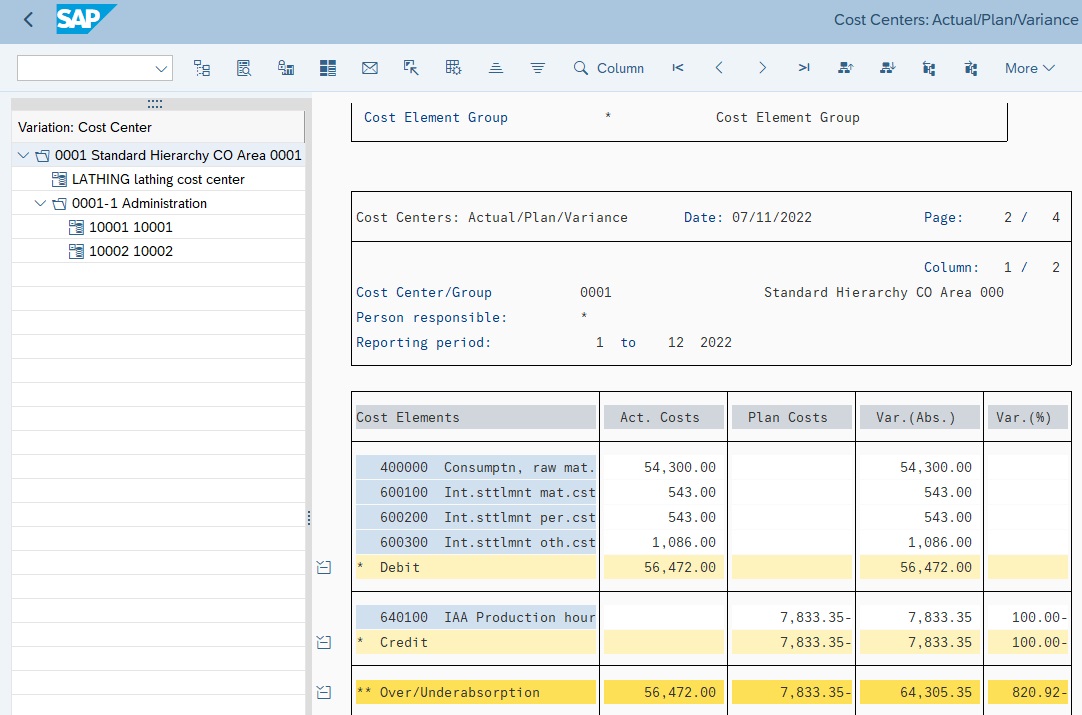

Figure 6 : Standard Cost Center Reporting

We look at standard reports in detail, including Cost Center Reporting as shown in Figure 6.

We analyze summarization reporting, including product drilldown reports.

We explore both classic reports and tools and SAP Fiori apps.

Chapter 7 Future Direction of Variance Analysis

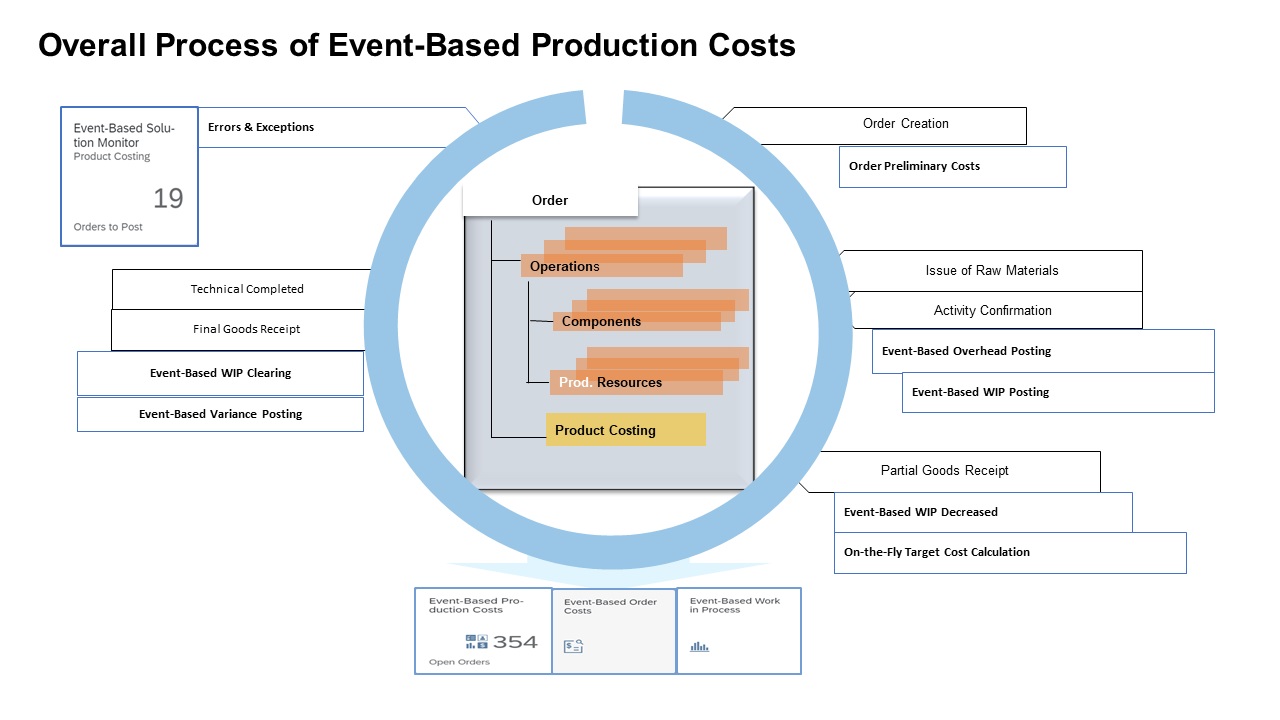

We show how SAP is moving away from calculating production variances at period end toward a new approach that calculates them with every final goods receipt, known as event-based variance analysis, as shown in Figure 7.

Figure 7: Event-Based Production Cost Cycle

Chapter 7 explains scrap and mixed price variances.

Chapters 1 to 6 are written and illustrated based on an on-premise SAP S/4HANA 2021 system.

Chapter 7 discusses new options for variance analysis delivered with SAP S/4HANA Cloud when you use scope item 3F0 (Event-Based Production Cost Posting) and SAP S/4HANA 2022, with the business function for universal parallel accounting.

Continue Reading: Production Variance Analysis in SAP S/4HANA

Glossary

We cover many terms in this book that are relevant to variance analysis. Let's review them:

Activity Input Planning

Just as cost centers can provide planned output services based on activity quantities with Transaction KP26, you can plan cost center activity input quantities from other cost centers with activity input planning using Transaction KP06.

Actual Costing

Actual costing determines what portion of the variance is debited to the next-highest level using material consumption. All purchasing and manufacturing difference postings are allocated upward through the BOM to assemblies and finished goods. Variances can be rolled up over multiple production levels and company codes to the finished product.

Actual Costs

Actual costs debit a product cost collector or manufacturing order during business transactions, for example, general ledger account postings, inventory goods movements, internal activity allocations, and overhead calculation.

Allocation Structure

An allocation structure allocates the costs incurred for a sender by cost element or cost element group, and it is used for settlement and assessment. An assignment maps a source cost element group to a settlement general ledger account.

Alternative Bill of Materials

There can be multiple methods of manufacturing an assembly, and many possible bills of materials (BOMs). The alternative BOM allows you to identify one BOM in a BOM group.

Alternative Hierarchy

While there can only be one cost center standard hierarchy, you can create as many alternative hierarchies as you like. You create an alternative hierarchy by creating cost center groups.

Alternative Unit Of Measure

This is a unit of measure defined in addition to the base unit of measure. Examples of alternative units of measure include order unit (purchasing), sales unit, and unit of issue.

Apportionment Method

An apportionment method distributes the total costs of a joint production process to the primary products. The costs of the individual primary products may vary. They are apportioned by means of an apportionment structure.

Apportionment Structure

An apportionment structure defines how costs are distributed to co-products. The system uses the apportionment structure to create a settlement rule that distributes costs from an order header to the co-products. For each co-product, the system generates a further settlement rule that assigns the costs distributed to the order item to stock.

Assembly Scrap

Assembly scrap is the percentage of assembly quantity that does not meet required quality standards. Assembly scrap is an output scrap because it increases the planned output quantity of items in the production process. You plan assembly scrap in the MRP 1 view using the Net ID checkbox in the Basic Data tab of a BOM item.

Automatic Account Assignment

Automatic account assignment allows you to set a default cost center per general ledger account per plant.

Backflush

Backflushing is the automatic posting of a goods issue for components in an order during confirmation. It reduces the amount of work in warehouse management, especially for low-value parts. The material components from the BOM are assigned to operations in the routing.

Base Quantity

All component quantities in a BOM relate to the base quantity. You increase the accuracy of component quantities by increasing the base quantity, similar in concept to the price unit.

Base Unit of Measure

Material stocks are managed in the base unit of measure. The system converts all quantities you enter in other units of measure (alternative units of measure) to the base unit of measure.

Bill of Material

A bill of material (BOM) is a structured hierarchy of components necessary to build an assembly. BOMs, and purchasing info records allow cost estimates to calculate material costs of assemblies.

BOM Application

A BOM application is a costing variant component for automatic determination of alternative BOMs.

BOM Group

A BOM group is a collection of BOMs for a product or number of similar products.

BOM Item Component Quantity

The quantity of a BOM item that is entered in relation to the base quantity of the product.

BOM Item Status

Six indicators, such as costing relevancy, are contained in the Status/Long Text tab of a BOM item.

BOM Status

This controls the current processing status of the BOM. For example, a BOM may have a default status of not active when initially created, which then may be changed to active when the BOM is available for use in material requirements planning (MRP) and released for planned orders.

BOM Usage

This determines a section of your company, such as production, engineering, or costing. You define which item statuses can be used in each BOM usage; for example, all items in BOMs with a certain usage may be relevant to production.

Bulk Material

Bulk materials are not relevant for costing in a cost estimate and are expensed

directly to a cost center. The Bulk Material checkbox is maintained in the MRP 2 view and the BOM item. If a material is always used as a bulk material, set the indicator in the material master. If a material is only used as a bulk material in individual cases, set the indicator in the BOM item, which has a higher priority.

Calculation Base

A calculation base is a group of cost elements to which overhead is applied. The calculation base is a component of a costing sheet, which summarizes the rules for allocating overhead.

Chart of Accounts

A chart of accounts is a group of general ledger accounts assigned to each company code. This chart of accounts is the operative chart of accounts used in both financial and cost accounting. All companies within the one controlling area must have the same operative chart of accounts. Other charts of accounts include the country-specific chart of accounts required by individual country legal requirements and the group chart of accounts required by consolidation reporting.

Company Code

A company code is the smallest organizational unit of financial accounting for

which a complete self-contained chart of accounts can be drawn up for external reporting.

Component Scrap

Component scrap is the percentage of component quantity that does not meet the required quality standards before being inserted into the production process. The plan quantity of components is increased. Component scrap is an input scrap because it is detected before use in the production process. You can plan component scrap in the MRP 4 view and the Basic Data tab of the BOM item. An entry in the BOM item field takes priority over an entry in the material master MRP 4 view.

Condition

Conditions are stipulations agreed upon with vendors, such as prices, discounts, surcharges, freight, duty, and insurance. You maintain purchasing conditions in quotations, purchasing info records, outline agreements, and orders.

Condition Technique

The condition technique determines the purchase price by considering all the relevant pricing elements, including formulating rules and requirements.

Condition Type

A condition type is a key that identifies a condition. It indicates, for example, whether the system applies a price, a discount, a surcharge, or other pricing, such as freight costs and sales taxes.

Confirmation

A confirmation documents the processing status of orders, operations, and individual capacities. You specify the operation yield, scrap and rework quantity, the activity quantity, the work center, and who operated.

Consignment Material

Consignment occurs when a vendor maintains a stock of materials at a customer site. The vendor retains ownership of the materials until they are withdrawn from the consignment stores.

Cost Center

A cost center is master data that identifies where the cost occurred. A responsible person assigned to the cost center analyzes and explains cost center variances at period end.

Cost Component

A cost component identifies costs of similar types, such as material, labor, and overhead costs by grouping together cost elements in the cost component structure.

Cost Component Group

Cost component groups allow you to display cost components in standard reports. In the simplest implementation, you create a cost component group for each cost component and assign each group to a corresponding cost component. You assign cost component groups as columns in cost estimate list reports and costed multilevel BOMs.

Cost Component Split

The cost component split is the combination of cost components that makes up the total cost of a material. For example, if you need to view three cost components (material, labor, and overhead) for your reporting requirements, the combination of these three cost components represents the cost component split.

Cost Component Structure

You define which cost components make up a cost component split by assigning them to a cost component structure. Within the cost component structure, you assign cost elements and origin groups to cost components.

Cost Component View

Each cost component is assigned to a cost component view. When you display a cost estimate, you can choose a cost component view, which filters the cost components displayed in the cost estimate.

Cost Element

Cost elements are included as part of a general ledger account. Primary cost elements identify external costs, while secondary cost elements identify costs allocated within controlling, such as activity allocations from cost centers to manufacturing orders.

Cost Estimate

A cost estimate calculates the plan cost to manufacture a product or purchase a component. It determines material costs by multiplying BOM quantities by the standard price, labor costs by multiplying operation standard quantities by plan activity price, and overhead by costing sheet configuration.

Costed Multilevel BOM

A costed multilevel BOM is a hierarchical overview of the values of all items of a costed material according to the material?s costed quantity structure (BOM and routing). You display a costed multilevel BOM on the left side of a cost estimate screen. You can also view a costed multilevel BOM separately with Transaction CK86_99.

Event-Based Processing

As of SAP S/4HANA release 2022, event-based processing is available, where goods movements and confirmations represent events that trigger the calculation of overhead according to the costing sheet. Then, depending on the status of the order, this triggers either the posting of a journal entry for the work in process (WIP) or the cancellation of any existing WIP and the calculation of production variances.

Goods Issue

A goods issue is the movement (removal) of goods or materials from inventory to manufacturing or to a customer. When goods are issued, it reduces the number of stock in the warehouse.

GR/IR

GR/IR is the SAP process to execute the three-way match- purchase order, Material Receipt, as well as vendor invoice. You use a clearing account to record the offset of the Goods Receipt (GR) and Invoice Receipt (IR) postings. As soon as completely processed, the postings in the cleaning account balance.

Internal Order

An internal order monitors costs and revenue of an organization for short- to-medium-term jobs. You can carry out planning at a cost element and detailed level, and budgeting at an overall level with availability control.

Long-Term Planning

Long-term planning allows you to enter medium- to longer-term production plans, and simulate future production requirements with long-term MRP. You can determine future purchasing requirements for vendor RFQs, update purchasing info records, and transfer planned activity requirements to cost center accounting.

Margin Analysis

Margin Analysis is the refined version of Account-Based COPA. The Universal Journal combines financial and managerial accounting and directly records all dimensions, including custom fields. Margin Analysis provides consistent financial information without any reconciliation needs and a financial audit trail. All innovations developed for the Universal Journal are immediately available within Margin Analysis. A consistent approach ensures common usage of ledgers, currencies, valuations, predictions, and simulations and their availability in planning and reporting.

Master Data

Master data is information that stays relatively constant over long periods of time. For example, purchasing info records contain vendor information such as a business name, which usually doesn't change.

Material Master

A material master contains all the information required to manage a material. Information is stored in views, each corresponding to a department or area of business responsibility. Views conveniently group information together for users in different departments, such as sales and purchasing.

Process Order

A process order is a manufacturing order used in process industries. A master recipe and materials list are copied from master data to the order. A process order contains operations divided into phases. A phase is a self-contained work step that defines the detail of one part of the production process using a primary resource.

In process manufacturing, only phases are costed, not operations. A phase is assigned to a subordinate operation and contains standard activity values, which are used to determine dates, capacity requirements, and costs.

Procurement Alternative

A procurement alternative represents one of a number of different ways of procuring a material. You can control the level of detail in which the procurement alternatives are represented through the controlling level. Depending on the processing category, there are single-level and multilevel procurement alternatives. For example, a purchase order is single-level procurement, while production is multilevel procurement.

Production Order

A production order is used for discrete manufacturing. A BOM and routing are copied from master data to the order. A sequence of operations is supplied by the routing, which describes how to carry out work-steps.

An operation can refer to a work center at which it is to be performed. An operation contains planned activities required to carry out the operation. Costs are based on the material components and activity price multiplied by a standard value.

Product Drilldown Reports

Product drilldown reports allow you to slice and dice data based on characteristics such as product group, material, plant, cost component, and period. Product drilldown reports are based on predefined summarization levels and are relatively simple to set up and run.

Production Variance

Production variance is a type of variance calculation based on the difference between net actual costs debited to the order and target costs based on the preliminary cost estimate and quantity delivered to inventory. You calculate production variance with the target cost version 1. Production variances are for information only and are not relevant for settlement.

Production Version

A production version determines which alternative BOM is used and which task list/master recipe to produce a material or create a master production schedule. You can have several production versions for one material for various validity periods and lot-size ranges.

Purchase Price Variance

When raw materials are valued at the standard price, a purchase price variance will post during goods receipt if the goods receipt or invoice price is different from the material standard price.

Profitability Analysis

Costing-based profitability analysis enables you to evaluate market segments, which can be classified according to products, customers, orders (or any combination of these), or strategic business units, such as sales organizations or business areas concerning your company's profit or contribution margin.

Profit Center

SAP Profit Center is a management-oriented organizational unit used for internal controlling purposes. Segmenting a company into profit centers allows us to analyze and delegate responsibility to decentralized units.

Purchasing Info Record

A purchasing information record stores all the information relevant to procuring a material from a vendor. It contains the Purchase Price field, which the standard cost estimate searches for when determining the purchase price.

Raw Materials

Raw materials are always procured externally and then processed. A material master record of this type contains purchasing data but not sales.

Routing

A routing is a list of tasks containing standard activity times required to perform operations to build an assembly. Routings, together with planned activity prices, provide cost estimates with the information necessary to calculate product labor and activity costs.

Sales and Operations Planning

Sales and operations planning S&OP allows you to enter a sales plan, convert it to a production plan, and transfer the plan to long-term planning.

S&OP is slowly being replaced by SAP Integrated Business Planning for Supply Chain (SAP IBP), which supports all S&OP features.